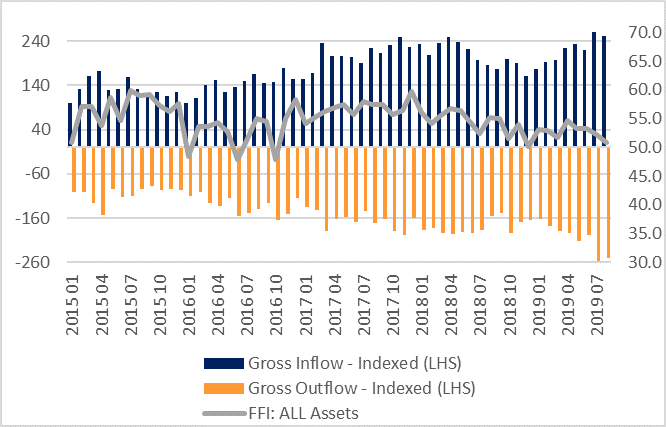

Flows into UK-based funds slumped to their second-lowest level in three years in August according to the latest Fund Flow Index (FFI) from Calastone, the largest global funds transaction network. Across all asset types, inflows were down, or there were outright outflows. As a result, UK investors added just £640m to their holdings, well below the long-run £2.4bn net monthly inflow. Over the last three years, only December 2018, when tumultuous stock markets were rocked by the intensification of global trade tensions, has seen weaker figures. The low level of inflows had nothing to do with the summer holiday season either, as the total volume of trading was well above the average for the year-to-date and for the last few years (see figure 1).

Figure 1: August trading volumes were high

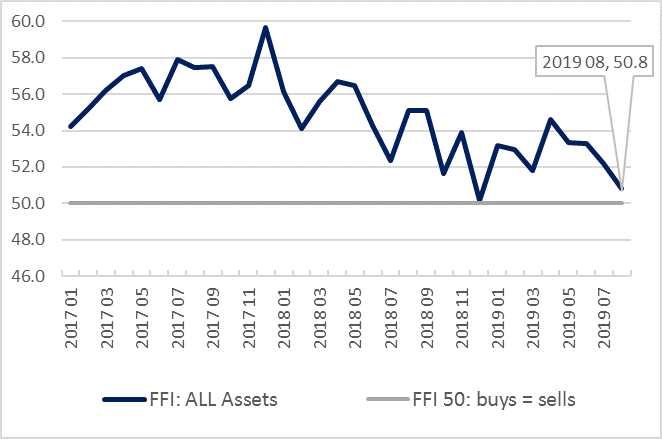

Figure 2: FFI: All Assets

Figure 2: FFI: All Assets

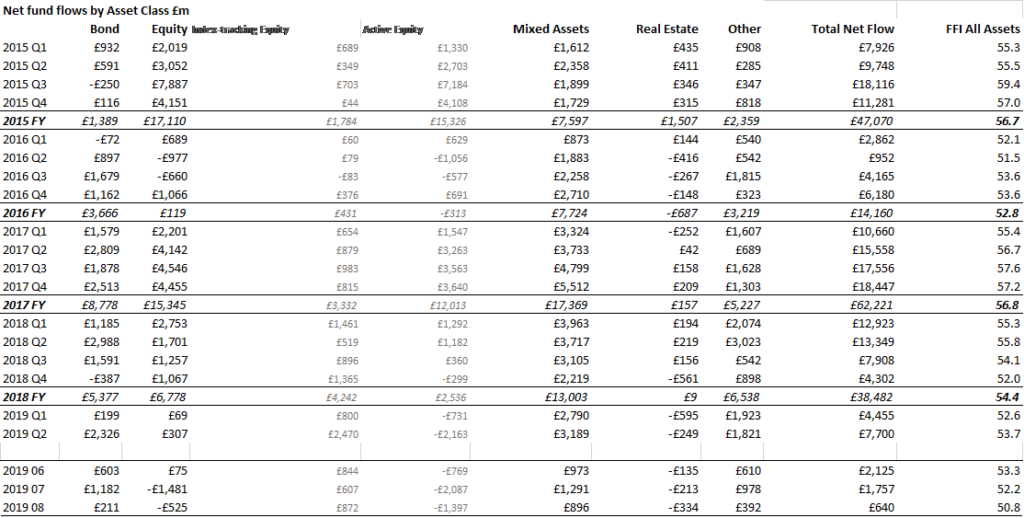

Equity funds were hit hardest. They saw investors sell down £525m of their holdings, while real-estate funds suffered their biggest outflows of the year so far, losing £334m. Even fixed-income funds, which have benefitted strongly all year from a flight to safety saw net inflows drop by over 80% month-on-month, down to just £211m, though that still meant they accounted for one third of all inflows, well above their long-run share of the total. The Calastone all asset FFI fell to 50.8, barely above the neutral 50 mark (see figure 2).

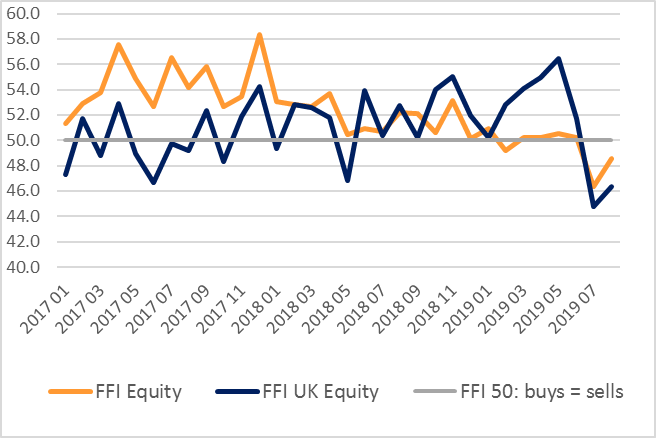

Among equity funds, UK-equity funds were easily the hardest hit, accounting for three-fifths of all the outflows. £306m fled the sector as investors shunned increasingly cheap UK valuations in growing alarm at political developments in the country and as the economic news darkened. The government’s decision to suspend Parliament which some argue was intended to head off MPs’ attempts to prevent a no-deal Brexit caused a spike in activity. One quarter of the month’s net selling in UK equity funds coincided with the announcement, on a day when most other kinds of equity funds enjoyed modest inflows. Separately, the inversion of the UK yield curve sparked one fifth of the month’s outflows.

Figure 3: FFI: UK equity v FFI: Equity

Equity funds were hit hardest. They saw investors sell down £525m of their holdings, while real-estate funds suffered their biggest outflows of the year so far, losing £334m. Even fixed-income funds, which have benefitted strongly all year from a flight to safety saw net inflows drop by over 80% month-on-month, down to just £211m, though that still meant they accounted for one third of all inflows, well above their long-run share of the total. The Calastone all asset FFI fell to 50.8, barely above the neutral 50 mark (see figure 2).

Among equity funds, UK-equity funds were easily the hardest hit, accounting for three-fifths of all the outflows. £306m fled the sector as investors shunned increasingly cheap UK valuations in growing alarm at political developments in the country and as the economic news darkened. The government’s decision to suspend Parliament which some argue was intended to head off MPs’ attempts to prevent a no-deal Brexit caused a spike in activity. One quarter of the month’s net selling in UK equity funds coincided with the announcement, on a day when most other kinds of equity funds enjoyed modest inflows. Separately, the inversion of the UK yield curve sparked one fifth of the month’s outflows.

Figure 3: FFI: UK equity v FFI: Equity

The FFI: UK Equity was just 46.3 for the month, well below the neutral mark. Equity income funds, whose assets are largely invested in UK shares too, saw a further £273m of outflows, the 28th consecutive month that money has left the sector. European equity funds shed £230m. Global funds and those focused on North America enjoyed modest inflows from bargain hunters making the most of down days for the financial markets and looking for somewhere to switch to.

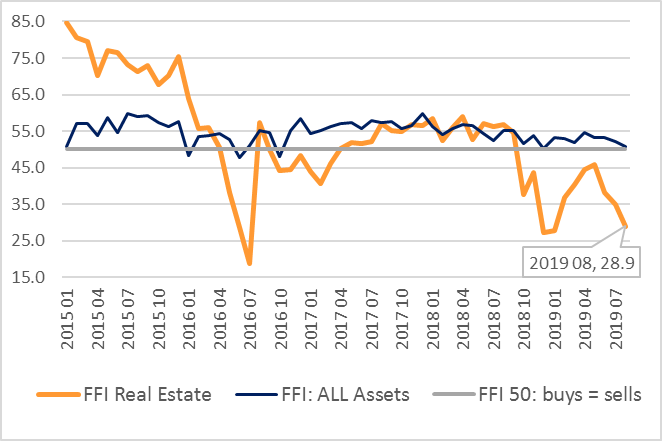

Political events in the UK are hitting real-estate funds too, as are growing fears of recession. August’s £334m outflow was the second-worst month for property funds ever, and marked a record 11th consecutive month of outflows. Investors have now withdrawn £2.0bn from these funds since last October. Outflows almost tripled when the government sought royal assent to prorogue Parliament, compared to the previous two-week average. The FFI: Real Estate fell to an extremely negative 28.9.

Figure 4: FFI: Real Estate

The FFI: UK Equity was just 46.3 for the month, well below the neutral mark. Equity income funds, whose assets are largely invested in UK shares too, saw a further £273m of outflows, the 28th consecutive month that money has left the sector. European equity funds shed £230m. Global funds and those focused on North America enjoyed modest inflows from bargain hunters making the most of down days for the financial markets and looking for somewhere to switch to.

Political events in the UK are hitting real-estate funds too, as are growing fears of recession. August’s £334m outflow was the second-worst month for property funds ever, and marked a record 11th consecutive month of outflows. Investors have now withdrawn £2.0bn from these funds since last October. Outflows almost tripled when the government sought royal assent to prorogue Parliament, compared to the previous two-week average. The FFI: Real Estate fell to an extremely negative 28.9.

Figure 4: FFI: Real Estate

The flood of UK capital into funds domiciled within the EU remained strong in August. While UK-UK funds inflows of £640m across all asset classes were three-quarters below their post-referendum average in August, UK-offshore funds enjoyed £1.6bn of inflows, only a tenth below average over the same period.

Edward Glyn, head of global markets at Calastone said, “Confidence is ebbing away, and investors are voting with their feet. Only the lowest risk categories of funds saw inflows in August. Even though equity outflows were a little smaller than in July, they were still strongly negative, with UK assets suffering the worst. UK political risk now combines with economic risk, so almost no matter how cheap UK asset valuations become relative to peers elsewhere, there is little appetite to buy them. The inversion of the UK yield curve, which signals the possibility of recession ahead, has only intensified concern. The flow of funds offshore expresses a further dimension of aversion to the UK – this is not about the asset classes those funds are invested in, but more about investor concerns over how the UK regulatory environment will handle the disruption caused by Brexit.

Fixed-income funds have been benefitting from the flight from risker assets, but the sharp drop in inflows in August is an acknowledgment that even this perceived safe haven may not protect capital when bond prices are so high and yields in some parts of the world negative, including at the long end of the curve.”

The flood of UK capital into funds domiciled within the EU remained strong in August. While UK-UK funds inflows of £640m across all asset classes were three-quarters below their post-referendum average in August, UK-offshore funds enjoyed £1.6bn of inflows, only a tenth below average over the same period.

Edward Glyn, head of global markets at Calastone said, “Confidence is ebbing away, and investors are voting with their feet. Only the lowest risk categories of funds saw inflows in August. Even though equity outflows were a little smaller than in July, they were still strongly negative, with UK assets suffering the worst. UK political risk now combines with economic risk, so almost no matter how cheap UK asset valuations become relative to peers elsewhere, there is little appetite to buy them. The inversion of the UK yield curve, which signals the possibility of recession ahead, has only intensified concern. The flow of funds offshore expresses a further dimension of aversion to the UK – this is not about the asset classes those funds are invested in, but more about investor concerns over how the UK regulatory environment will handle the disruption caused by Brexit.

Fixed-income funds have been benefitting from the flight from risker assets, but the sharp drop in inflows in August is an acknowledgment that even this perceived safe haven may not protect capital when bond prices are so high and yields in some parts of the world negative, including at the long end of the curve.”

Methodology

Calastone analysed over a million buy and sell orders every month from January 2015, tracking monies from IFAs, platforms and institutions as they flow into and out of investment funds. Data is collected until the close of business on the last day of each month. A single order is usually the aggregated value of a number of trades from underlying investors passed for example from a platform via Calastone to the fund manager. In reality, therefore, the index is analysing the impact of many millions of investor decisions each month.

More than two thirds of UK fund flows by value pass across the Calastone network each month. All these trades are included in the FFI. To avoid double-counting, however, the team has excluded deals that represent transactions where funds of funds are buying those funds that comprise the portfolio. Totals are scaled up for Calastone’s market share.

A reading of 50 indicates that new money investors put into funds equals the value of redemptions (or sales) from funds. A reading of 100 would mean all activity was buying; a reading of 0 would mean all activity was selling. In other words, £1m of net inflows will score more highly if there is no selling activity, than it would if £1m was merely a small difference between a large amount of buying and a similarly large amount of selling.

Calastone’s main FFI All Assets considers transactions only by UK-based investors, placing orders for funds domiciled in the UK. The majority of this capital is from retail investors. Calastone also measures the flow of funds from UK-based investors to offshore-domiciled funds. Most of these are domiciled in Ireland and Luxembourg. This is overwhelmingly capital from institutions; the larger size of retail transactions in offshore funds suggests the underlying investors are higher net worth individuals.

Methodology

Calastone analysed over a million buy and sell orders every month from January 2015, tracking monies from IFAs, platforms and institutions as they flow into and out of investment funds. Data is collected until the close of business on the last day of each month. A single order is usually the aggregated value of a number of trades from underlying investors passed for example from a platform via Calastone to the fund manager. In reality, therefore, the index is analysing the impact of many millions of investor decisions each month.

More than two thirds of UK fund flows by value pass across the Calastone network each month. All these trades are included in the FFI. To avoid double-counting, however, the team has excluded deals that represent transactions where funds of funds are buying those funds that comprise the portfolio. Totals are scaled up for Calastone’s market share.

A reading of 50 indicates that new money investors put into funds equals the value of redemptions (or sales) from funds. A reading of 100 would mean all activity was buying; a reading of 0 would mean all activity was selling. In other words, £1m of net inflows will score more highly if there is no selling activity, than it would if £1m was merely a small difference between a large amount of buying and a similarly large amount of selling.

Calastone’s main FFI All Assets considers transactions only by UK-based investors, placing orders for funds domiciled in the UK. The majority of this capital is from retail investors. Calastone also measures the flow of funds from UK-based investors to offshore-domiciled funds. Most of these are domiciled in Ireland and Luxembourg. This is overwhelmingly capital from institutions; the larger size of retail transactions in offshore funds suggests the underlying investors are higher net worth individuals.