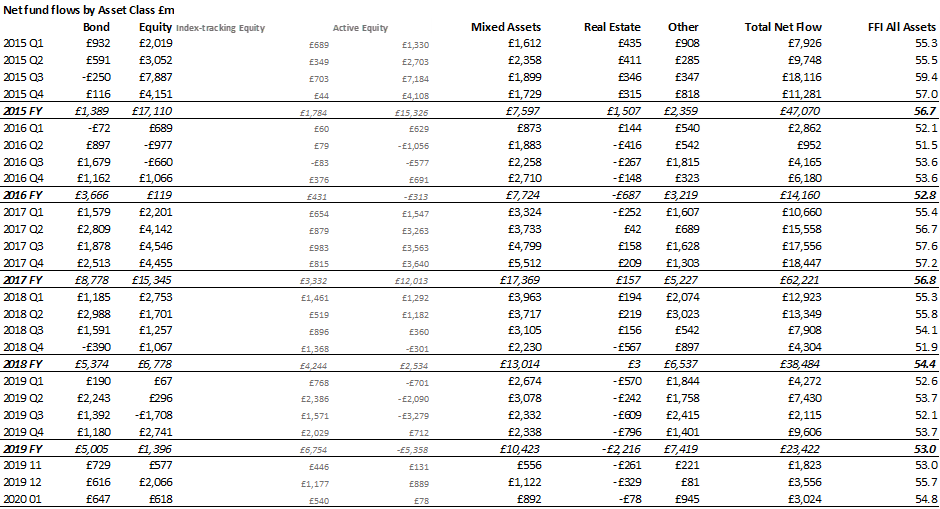

Equity fund inflows dropped sharply in January, failing to maintain the momentum generated by a surge of inflows that gave equity funds their best month in two years in December 2019. The latest Fund Flow Index (FFI) from Calastone, the largest global funds network, shows that net inflows fell by more than two thirds to £618m in January. Two-fifths of this new capital flowed into UK equity funds, though the inflow to UK equities dropped by three quarters month on month, as the post-election bounce in sentiment faded and coronavirus news began to hit.

Nine-tenths of January’s overall net equity inflow went into index funds, with the remainder flowing into active funds. This means that while the value of capital subscribed for passive equity funds merely halved month-on-month, it dropped 93% for active equity funds. The latter are much more sensitive to changes in sentiment, so the negative coronavirus news hit inflows here much harder. The small £78m inflow for active funds belied how confidence drained away as the month progressed (see below).

The total trading volume (ie the value of buys plus the value of sells) increased slightly in January (up 3.2%) to £16.1bn, the second-highest month since April 2018, thanks largely to a sharp increase in selling activity. The drop in net inflows in January was caused mainly by this higher selling activity. Slower buying activity also contributed to the decline in net inflows, but to a much lesser extent.

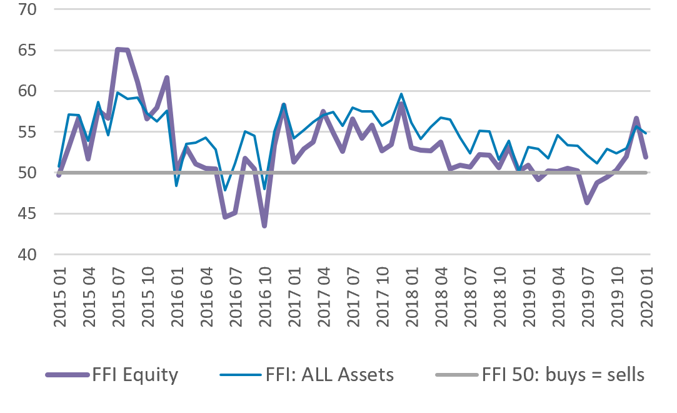

Lower inflows on higher overall volumes dragged Calastone’s FFI: Equity down to 51.9 in January (a neutral 50 means the value of buys equals the value of sells), still in positive territory, but well below the bullish reading of 56.7 in December.

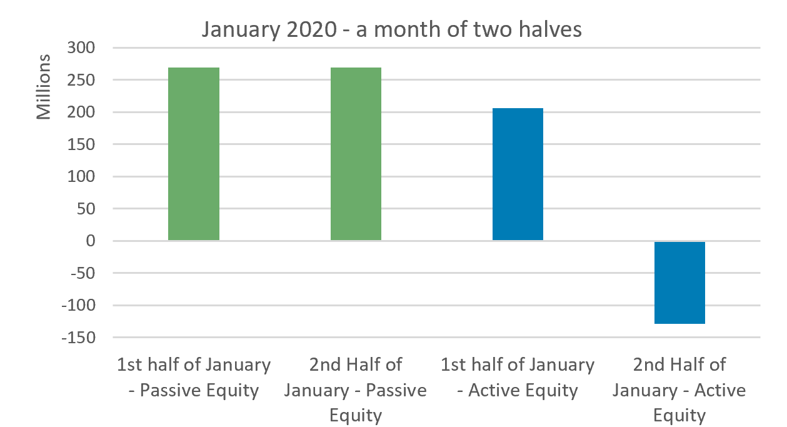

It was, however, a month of two halves. As news of the coronavirus outbreak began to emerge, investor confidence dropped. In the first half of the month, before the virus had begun to make the news, equity funds saw £475m of inflows, but this slowed to just £141m in the second half of the month as investors pared back the optimism that more positive news on the global economy had instilled in December. This was a distinctly ‘active equities’ phenomenon as investors absorbed the likely hit to industrial sectors like airlines, and regions like Asia. Index funds were relatively unaffected, but active funds saw inflows of £206m in the first half of the month turn to outflows of £128m in the second half, after the coronavirus news hit. Among the other main asset classes (fixed income, multi-asset and real estate) flows were broadly balanced over the course of the month.

Asia focussed funds were indeed the worst hit, suffering their worst month in two-and-a-half years. A net £61m left the sector in January, the weakest since July 2016.

Among the other main asset classes, inflows to the relative safe haven of fixed income funds rose and were 50% higher than their 12-month average, while outflows from property funds slowed to their lowest level since May 2019 (separate property press release available on request). Inflows to multi-asset funds fell month-on-month too.

Edward Glyn, head of global markets at Calastone said: “Stock markets have swooned since the coronavirus hit, as share prices have been marked down sharply in the expectation of slower global growth. The response of fund investors shows how the virus was most impactful for fund categories where its effect will be greatest, like Asia. But active funds also faced problems. The investor verdict on active equity funds was swift and decisive but passive funds were untouched. In times when confidence is weak, active funds bear the brunt of selling, while passive funds are relatively unscathed. By the same token, a sudden upturn in confidence, like we saw in December, is far more positive for active funds. Passive funds are cemented into regular savings plans via ISAs and pensions so investors clearly do not tinker with their passive holdings that much. By contrast, they trade their active funds much more dynamically, responding quickly to market events as they happen.”

Nine-tenths of January’s overall net equity inflow went into index funds, with the remainder flowing into active funds. This means that while the value of capital subscribed for passive equity funds merely halved month-on-month, it dropped 93% for active equity funds. The latter are much more sensitive to changes in sentiment, so the negative coronavirus news hit inflows here much harder. The small £78m inflow for active funds belied how confidence drained away as the month progressed (see below).

The total trading volume (ie the value of buys plus the value of sells) increased slightly in January (up 3.2%) to £16.1bn, the second-highest month since April 2018, thanks largely to a sharp increase in selling activity. The drop in net inflows in January was caused mainly by this higher selling activity. Slower buying activity also contributed to the decline in net inflows, but to a much lesser extent.

Lower inflows on higher overall volumes dragged Calastone’s FFI: Equity down to 51.9 in January (a neutral 50 means the value of buys equals the value of sells), still in positive territory, but well below the bullish reading of 56.7 in December.

It was, however, a month of two halves. As news of the coronavirus outbreak began to emerge, investor confidence dropped. In the first half of the month, before the virus had begun to make the news, equity funds saw £475m of inflows, but this slowed to just £141m in the second half of the month as investors pared back the optimism that more positive news on the global economy had instilled in December. This was a distinctly ‘active equities’ phenomenon as investors absorbed the likely hit to industrial sectors like airlines, and regions like Asia. Index funds were relatively unaffected, but active funds saw inflows of £206m in the first half of the month turn to outflows of £128m in the second half, after the coronavirus news hit. Among the other main asset classes (fixed income, multi-asset and real estate) flows were broadly balanced over the course of the month.

Asia focussed funds were indeed the worst hit, suffering their worst month in two-and-a-half years. A net £61m left the sector in January, the weakest since July 2016.

Among the other main asset classes, inflows to the relative safe haven of fixed income funds rose and were 50% higher than their 12-month average, while outflows from property funds slowed to their lowest level since May 2019 (separate property press release available on request). Inflows to multi-asset funds fell month-on-month too.

Edward Glyn, head of global markets at Calastone said: “Stock markets have swooned since the coronavirus hit, as share prices have been marked down sharply in the expectation of slower global growth. The response of fund investors shows how the virus was most impactful for fund categories where its effect will be greatest, like Asia. But active funds also faced problems. The investor verdict on active equity funds was swift and decisive but passive funds were untouched. In times when confidence is weak, active funds bear the brunt of selling, while passive funds are relatively unscathed. By the same token, a sudden upturn in confidence, like we saw in December, is far more positive for active funds. Passive funds are cemented into regular savings plans via ISAs and pensions so investors clearly do not tinker with their passive holdings that much. By contrast, they trade their active funds much more dynamically, responding quickly to market events as they happen.”