Fund inflows rebounded in November as UK investors took advantage of the sharp drop in global stock markets at the end of October, according to the latest Fund Flows Index (FFI) from Calastone, the largest global funds transaction network. The new monthly index tracks orders representing millions of individual investor decisions, and is the most comprehensive, and up-to-date measure of UK fund flows (see methodology).

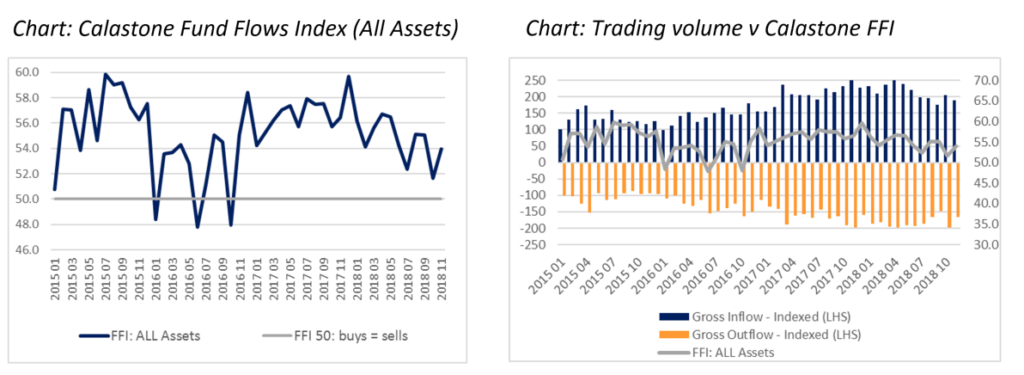

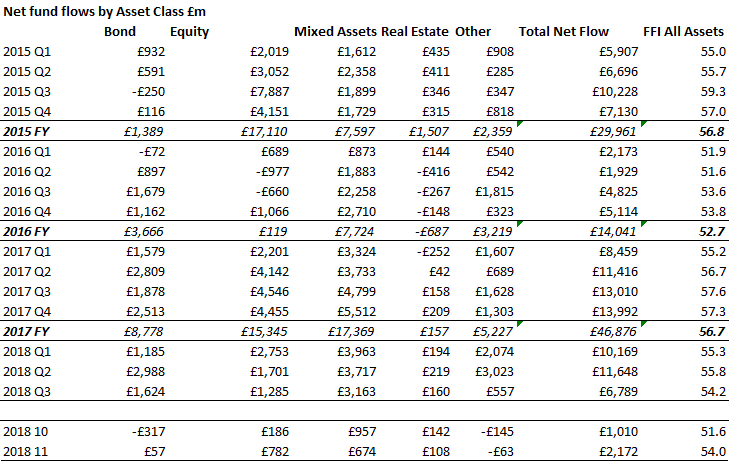

UK investors committed a net £2.2bn to funds in November, more than double October’s total. This took Calastone’s FFI to 54.0, up from the two-year low of 51.6 reached in October when sharp reversals hit global financial markets across a variety of asset classes. Even so, this still left the index in November below both its long-run average, and its average for the last twelve months (55.2 in both cases; 50 means inflows equal outflows). Total trading volumes (the sum of buying and selling) were also below the average for the last twelve months (down by a tenth), though this is set against a busy year of activity for investors.

If you would like to subscribe to receive the FFI, please click here

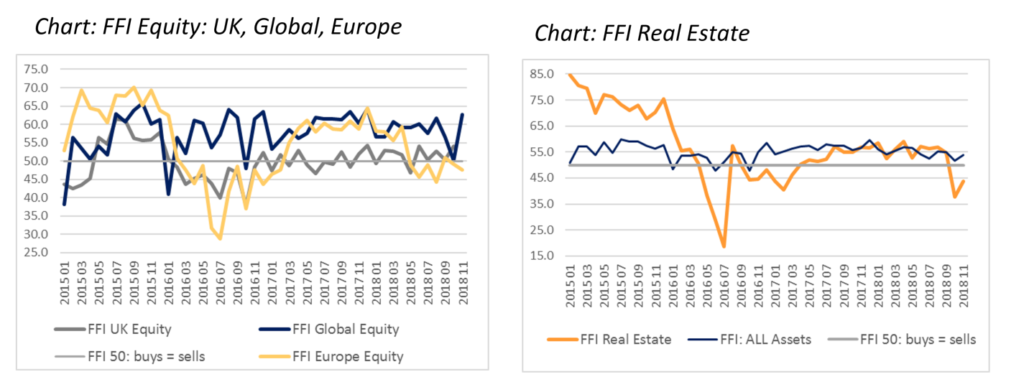

Equity funds had the best month since April, seeing £782m of net inflows. The FFI Equity rose to 52.9, its highest since January. Global funds accounted for the largest share, while North American equity funds saw the strongest net inflow in over a year (FFI North America 60.1), more than reversing net sales seen in October. Investors’ renewed enthusiasm for UK equities was sustained in November, but European equities remained out of favour as economic news from the eurozone continued to disappoint. Property funds saw a second consecutive month of outflows, taking net sales to £208m since the beginning of October, the worst performance since the aftermath of the Brexit referendum in 2016. The FFI Real Estate was just 43.8 in November, well below the neutral 50 mark.

Equity funds had the best month since April, seeing £782m of net inflows. The FFI Equity rose to 52.9, its highest since January. Global funds accounted for the largest share, while North American equity funds saw the strongest net inflow in over a year (FFI North America 60.1), more than reversing net sales seen in October. Investors’ renewed enthusiasm for UK equities was sustained in November, but European equities remained out of favour as economic news from the eurozone continued to disappoint. Property funds saw a second consecutive month of outflows, taking net sales to £208m since the beginning of October, the worst performance since the aftermath of the Brexit referendum in 2016. The FFI Real Estate was just 43.8 in November, well below the neutral 50 mark.

Despite the overall positive figures in November, the month was split clearly into two halves. In the first two weeks, fund flows were positive every day, but by the second half, renewed volatility in global markets meant investors withdrew capital on several occasions, only to jump back in when prices fell. For example, the 15th November saw heavy net selling as markets were steadily falling, but investors bought back enthusiastically six days later on the 21st, as markets touched the bottom. Total trading volumes were noticeably higher on these inflexion days than on less dramatic days, and most of the activity was in equity funds. Capital flowed out of property funds on every day except one in the second half of the month.

Inflows from UK investors to offshore funds remained stronger than those domiciled in the UK, a trend which Calastone attributes to nervousness about the regulatory status of UK-domiciled funds post-Brexit in March 2019. Offshore funds saw a net inflow of £1.5bn in November, with the FFI Offshore registering 55.6, in line with its post-referendum average and well ahead of pre-referendum levels.

Edward Glyn, Calastone’s Head of Global Markets, comments: “November has been a good month for fund flows but investors are much more skittish than the positive overall figures for the month suggest. We expect Q4 2018 to see the weakest fund flows since 2016. Asset prices are currently very volatile, so investors are watching the markets day by day, and dipping in and out in reaction to fast-changing news. Timing the markets is tricky even for professionals, but investors are clearly giving it a go to try to lock in short-term profits. Fund flows longer term are structurally positive, however, as investors aim to steadily build their savings.

Meanwhile, news flow for the real estate sector has been very poor recently amid concerns about asset values, culminating in the collapse of Intu Properties takeover talks. That seems to be making investors in property funds nervous, and is prompting outflows.”

Despite the overall positive figures in November, the month was split clearly into two halves. In the first two weeks, fund flows were positive every day, but by the second half, renewed volatility in global markets meant investors withdrew capital on several occasions, only to jump back in when prices fell. For example, the 15th November saw heavy net selling as markets were steadily falling, but investors bought back enthusiastically six days later on the 21st, as markets touched the bottom. Total trading volumes were noticeably higher on these inflexion days than on less dramatic days, and most of the activity was in equity funds. Capital flowed out of property funds on every day except one in the second half of the month.

Inflows from UK investors to offshore funds remained stronger than those domiciled in the UK, a trend which Calastone attributes to nervousness about the regulatory status of UK-domiciled funds post-Brexit in March 2019. Offshore funds saw a net inflow of £1.5bn in November, with the FFI Offshore registering 55.6, in line with its post-referendum average and well ahead of pre-referendum levels.

Edward Glyn, Calastone’s Head of Global Markets, comments: “November has been a good month for fund flows but investors are much more skittish than the positive overall figures for the month suggest. We expect Q4 2018 to see the weakest fund flows since 2016. Asset prices are currently very volatile, so investors are watching the markets day by day, and dipping in and out in reaction to fast-changing news. Timing the markets is tricky even for professionals, but investors are clearly giving it a go to try to lock in short-term profits. Fund flows longer term are structurally positive, however, as investors aim to steadily build their savings.

Meanwhile, news flow for the real estate sector has been very poor recently amid concerns about asset values, culminating in the collapse of Intu Properties takeover talks. That seems to be making investors in property funds nervous, and is prompting outflows.”

Methodology

Calastone analysed over a million buy and sell orders every month from January 2015, tracking monies from IFAs, platforms and institutions as they flow into and out of investment funds. Data is collected until the close of business on the last day of each month. A single order is usually the aggregated value of a number of trades from underlying investors passed for example from a platform via Calastone to the fund manager. In reality, therefore, the index is analysing the impact of many millions of investor decisions each month.

More than two thirds of UK fund flows by value pass across the Calastone network each month. All these trades are included in the FFI. To avoid double-counting, however, the team has excluded deals that represent transactions where funds of funds are buying those funds that comprise the portfolio. Totals are scaled up for Calastone’s market share.

A reading of 50 indicates that new money investors put into funds equals the value of redemptions (or sales) from funds. A reading of 100 would mean all activity was buying; a reading of 0 would mean all activity was selling. In other words, £1m of net inflows will score more highly if there is no selling activity, than it would if £1m was merely a small difference between a large amount of buying and a similarly large amount of selling.

Calastone’s main FFI All Assets considers transactions only by UK-based investors, placing orders for funds domiciled in the UK. The majority of this capital is from retail investors. Calastone also measures the flow of funds from UK-based investors to offshore-domiciled funds. This is overwhelmingly capital from institutions; the larger size of retail transactions in offshore funds suggests the underlying investors are higher net worth individuals.

Funds are categorised using a combination of Lipper and Calastone fund attributes. ETFs are not included in the analysis.

If you would like to subscribe to receive the FFI, please click here

Methodology

Calastone analysed over a million buy and sell orders every month from January 2015, tracking monies from IFAs, platforms and institutions as they flow into and out of investment funds. Data is collected until the close of business on the last day of each month. A single order is usually the aggregated value of a number of trades from underlying investors passed for example from a platform via Calastone to the fund manager. In reality, therefore, the index is analysing the impact of many millions of investor decisions each month.

More than two thirds of UK fund flows by value pass across the Calastone network each month. All these trades are included in the FFI. To avoid double-counting, however, the team has excluded deals that represent transactions where funds of funds are buying those funds that comprise the portfolio. Totals are scaled up for Calastone’s market share.

A reading of 50 indicates that new money investors put into funds equals the value of redemptions (or sales) from funds. A reading of 100 would mean all activity was buying; a reading of 0 would mean all activity was selling. In other words, £1m of net inflows will score more highly if there is no selling activity, than it would if £1m was merely a small difference between a large amount of buying and a similarly large amount of selling.

Calastone’s main FFI All Assets considers transactions only by UK-based investors, placing orders for funds domiciled in the UK. The majority of this capital is from retail investors. Calastone also measures the flow of funds from UK-based investors to offshore-domiciled funds. This is overwhelmingly capital from institutions; the larger size of retail transactions in offshore funds suggests the underlying investors are higher net worth individuals.

Funds are categorised using a combination of Lipper and Calastone fund attributes. ETFs are not included in the analysis.

If you would like to subscribe to receive the FFI, please click here