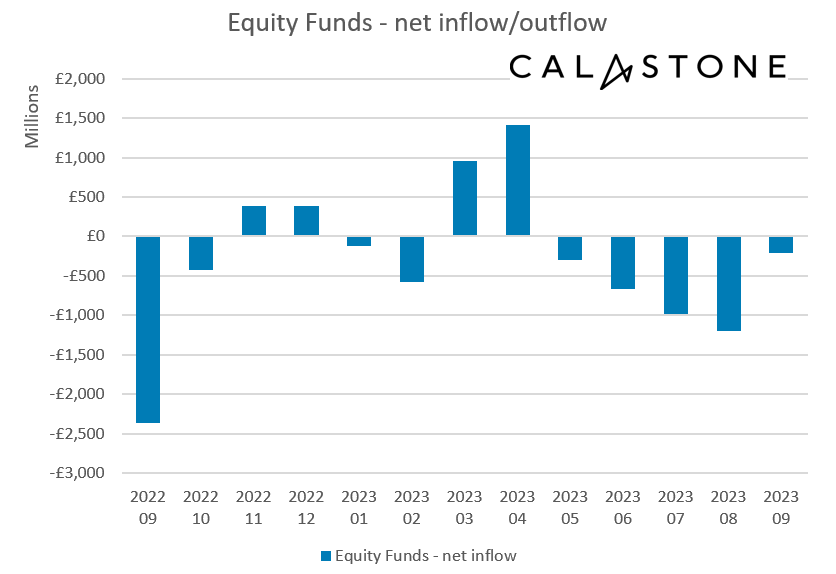

Equity funds were hit by a fifth consecutive month of outflows in September as the summer’s volatile bond markets forced a reappraisal of stock valuations, according to the latest Fund Flow Index from Calastone, the largest global funds network. Outflows of £206m from equity funds were, however, the least severe since February this year.

UK funds hit by largest outflows, but relative to their size US funds are seeing more selling pressure

Among the geographical sectors of equity funds, UK-focused funds shed the most – redemptions of £448m made September the 28th consecutive month of outflows for the sector. Meanwhile investors withdrew a net £285m from the much smaller North American fund sector. Relative to their overall size, however, North American funds have been hit roughly 40% harder by outflows over the last three months[1]. Income funds also suffered significant outflows, shedding £594m, their second-worst reading of the year after August.

ESG funds suffer 5th consecutive monthly outflows – investors increasingly turning their backs

ESG funds suffered a fifth consecutive month of outflows in what is now a clearly emerging trend. Investors redeemed £485m from their ESG equity holdings, almost half of which came from North American ESG funds.

Global funds remain the investor’s favourite, and emerging markets enjoy a moment in the sun

Global funds continue to lead the pack. They attracted £981m of new capital in September[2], while emerging markets continued their best run on Calastone’s record. Investors added £284m in September, taking the year-to-date total to £2.39bn.

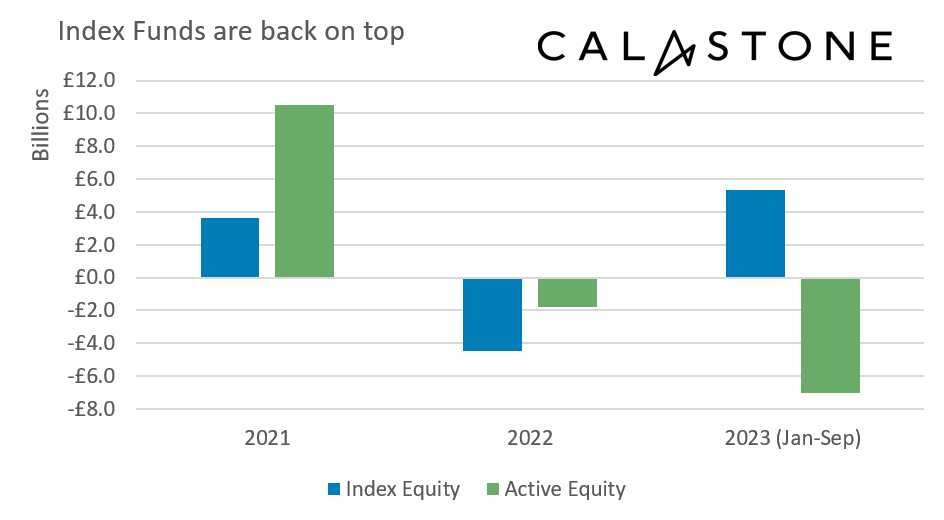

Index funds are back in vogue after losing out to active ones in 2021 and 2022

Equity index funds have returned to the fore in 2023 having lagged behind their active counterparts in 2021 and 2022. They enjoyed £1.10bn of inflows in September, driven mainly by inflows to global index funds. Active funds had their worst month in a year, with outflows of £1.30bn. Year-to-date inflows to passive funds of £5.35bn stand in stark contrast to outflows of £7.03bn from active ones. Active fund outflows are the most severe among UK, Income, North American, European and ESG funds both in September’s monthly figures and this year.

Fixed income funds see outflows in September as market volatility hits sentiment

Elsewhere, bond funds also suffered from volatile conditions in September, shedding £128m, while safe-haven and high-yielding money market funds continued to attract new capital – a net £189m in September.

Edward Glyn, head of global markets at Calastone commented: “The bond markets are in the driving seat at the moment. One moment, inflation coming in better than expected or central banks hitting pause on interest rates causes a bond market rally. The mathematical alchemy that links bond yields to stock market valuations, as well as investor hopes for a soft economic landing, give equities a boost. The next moment, policymakers take the punchbowl away with a warning that rates will stay high for the foreseeable future – bond yields surge and equity markets sag. Clear signs of sustained disinflation accompanied by a definitive turn in the rate cycle seem to be top of the wish list for market bulls at present.

“The distaste for UK equities is a structural trend that domestic and international investors are unwilling to break, despite attractive valuations, but outflows from North American funds only began in earnest with the bear market in 2022. Highly valued US equities, especially in the technology sector, are especially sensitive to rising bond yields – fund flows in and out of US equity funds have followed moves in the bond markets lately. Meanwhile, inflows to emerging markets in 2023 reflect attractive prices after very steep falls from their 2021 peak and accompany calmer emerging market bond yields this year.”

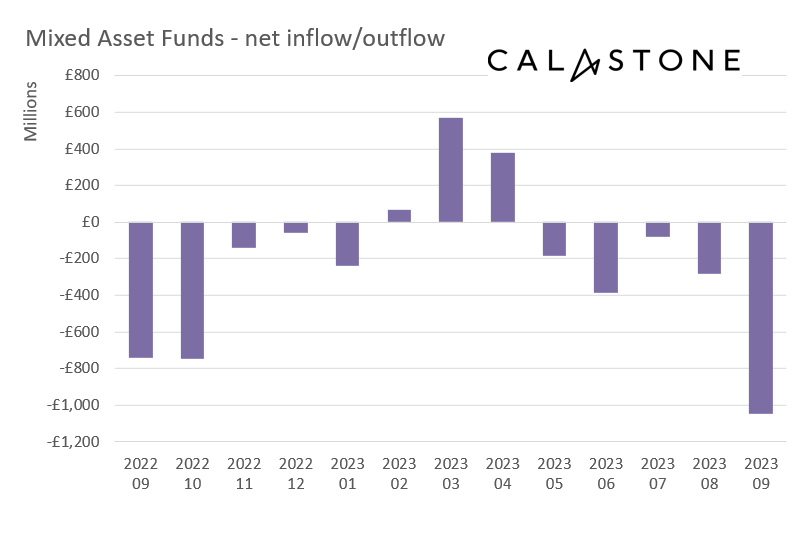

Mixed asset funds suffer worst month on record – risk/reward profile is no longer attractive

Mixed asset funds had their worst month on Calastone’s record, shedding £1.04bn. After five months of net selling this was the longest run of outflows from the sector Calastone has seen. Indeed, in the seven years between 2015 and 2021, only three months had ever seen outflows from mixed asset funds. Since the beginning of 2022, by contrast, eleven months have seen net selling, five of these since May this year.

Edward Glyn added: “The objective with mixed asset funds is to exploit the traditional inverse correlation between equities and bonds to generate better risk-adjusted returns. The trouble is that bond and equity markets have moved largely in tandem in the last eighteen months or so which is leading investors to question whether they can do better elsewhere for a similar risk profile. This reappraisal is clearly driving investors out the door. Mixed asset funds used to enjoy steady inflows month in, month out, as investors had them cemented into savings plans, but this no longer seems to be the case.”

[1] Over the last three months UK-focused funds have suffered outflows of £1.95bn and North American funds £1.55bn; UK equity AUM is £154bn and North America £85bn (source IA).

[2] September’s inflows took the inflow to global funds to £9.90bn year-to-date