Investment fund flows were the weakest in at least eight years in 2022, according to the latest Fund Flow Index from Calastone, the largest global funds network.

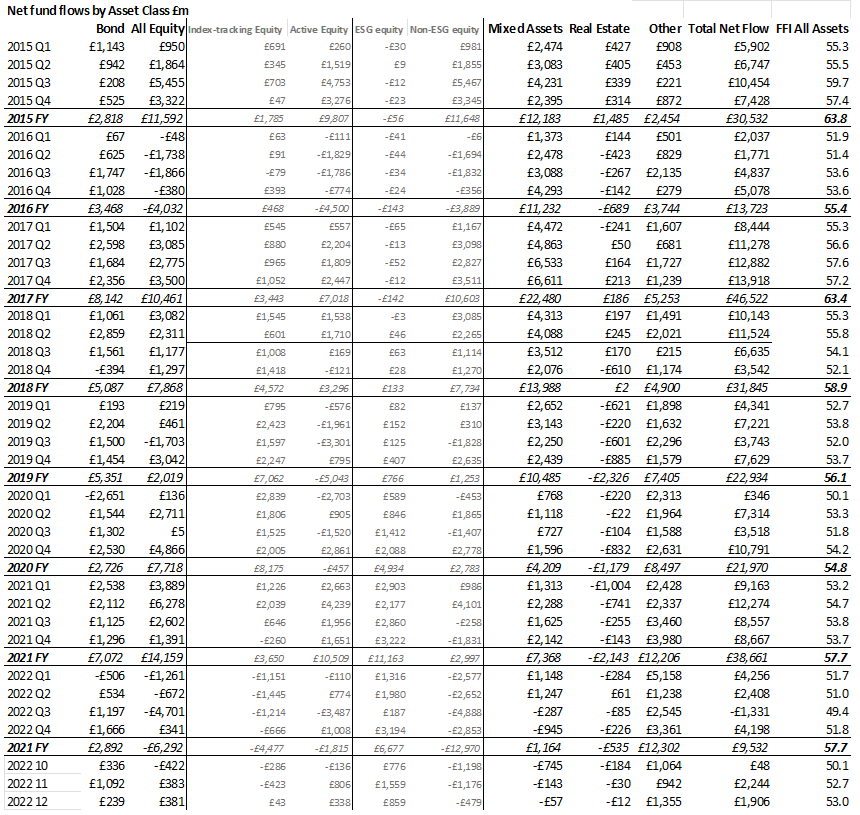

Equity funds suffered outflows of £6.29bn

Equity funds were hardest hit, shedding £6.29bn over the course of the year, three quarters of which flowed out in the third quarter. Within this diverse asset class some fund sectors were hit much harder than others.

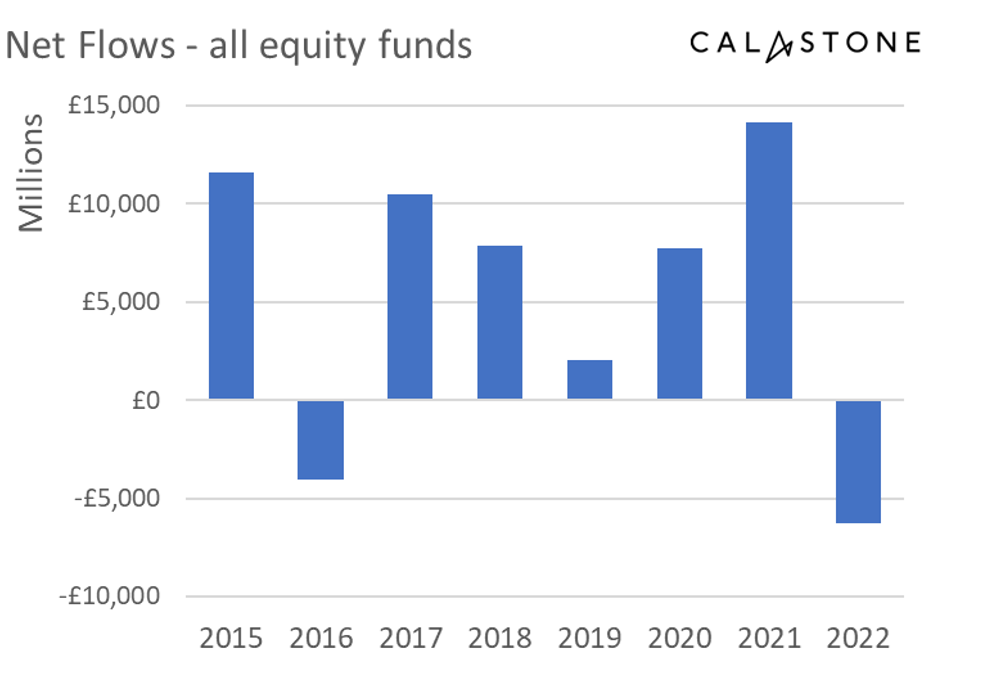

UK-focused funds hit hardest by far with record outflows of £8.38bn

Investors were unyielding in their shunning of UK-focused funds– during the year outflows totalled a record[1] £8.38bn, with every month seeing net selling continue. 2022 was the second consecutive year of outflows for UK-focused funds. Elsewhere, investors sold £2.65bn of European funds (a fourth consecutive year of net selling), a record £1.17bn of North American funds (the first year of outflows since 2016) and £1.00bn of Asia-Pacific funds.

Global funds enjoyed inflows – thanks to popularity of ESG

Global funds continued to attract new capital, however. Investors added a net £4.87bn, but this was thanks entirely to ESG strategies: global ESG equity funds attracted £6.35bn, while those without an ESG mandate shed £1.48bn. Emerging-market funds enjoyed inflows of £647m, while equity income funds had their best year on Calastone’s record, reflecting their defensive qualities in times of recession and higher interest rates. They still suffered outflows (-£427m for the year), but this compares to outflows more than ten times larger in each of 2020 and 2021 and far larger outflows in 2022 for non-income strategies.

[1] All references to records refer to Calastone’s eight-year data series, unless otherwise stated

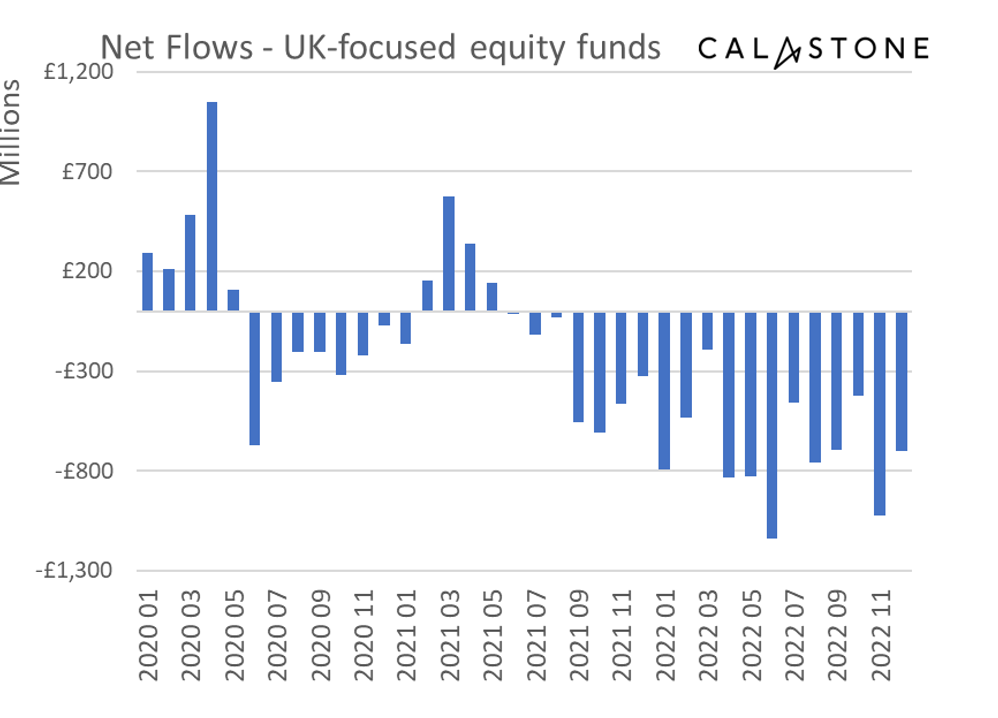

Passive funds suffered first year of outflows on record and fared worse than active for second consecutive year

It was a bad year for passive equity funds, which saw their first year of outflows on Calastone’s record. For the second year in a row they fared worse than their active counterparts. In 2022, passive funds shed £4.45bn, while active ones saw much smaller outflows of £1.82bn, despite being far larger by assets under management. Global index funds suffered the largest outflows of capital (-£3.26bn) while their active counterparts gathered net inflows of £8.13bn (much of which reflected the popularity of ESG).

Q4 saw optimism begin to return – equity funds saw inflows (though UK remains out of favour)

By November markets were buoyed by hopes that the cycle of rate increases from central banks around the world might be nearing the end. This meant tentative inflows to equity funds in November and December (see table in appendix), heavily focused on global funds (primarily ESG), but with modest interest in emerging markets and equity income too. Equity funds overall saw £381m of inflows in December. Investors still refused to touch UK-focused equity funds, however. December’s outflow was £701m.

Hopes of an end to the interest rate cycle spurred fixed income inflows in Q4, after a difficult first few months of 2022

Rising inflation and higher interest rates are negative for bond prices. Inflows continued to fixed income funds, but at £2.89bn for the year, they were sharply lower than the £7.07bn inflow in 2021, when rock bottom interest rates pushed bond prices higher. Investors were most positive on fixed income in the fourth quarter, adding a net £1.67bn. By this time, yields were significantly higher than at the beginning of the year (thanks to falling prices) so new investor capital into these funds will receive more interest income than at any point in the last 14 years. The inflows also indicate that investors have begun to anticipate an end to the rate-hike cycle and so positioned themselves for a potential bond-market rally.

Among other asset classes, mixed asset funds had their worst year on Calastone’s record attracting inflows of £1.16bn, while property funds saw outflows shrink by three quarters to £535m.

Edward Glyn, head of global markets at Calastone said: “2022 was a momentous year. The sudden flip by central banks from floods of liquidity and cheap money to a barrage of rate hikes aimed at taming rampant inflation turned asset markets upside down.

“There is a structural bias in the market towards fund inflows as we put money aside in our pensions and ISAs/savings plans, so such large outflows from equity funds in 2022 without a corresponding increase in other asset classes is a very large vote of no-confidence. Investors have sought out the safest havens they can find, taking refuge in cash and the perceived lower risk fund categories.

“Sentiment has improved markedly in recent weeks, but there is enormous uncertainty over the future course of interest rates and economic growth around the world and we may yet see the bear roar again before the bull market cycle can begin anew. The expectation that the UK economy will suffer the worst recession among major economies has prevented the current burst of optimism spreading to UK-focused funds, however.

“It’s tough for the industry. Fund management groups were hit with a double whammy – the supply of capital shrank as bond and equity markets fell, and the replenishment rate either reduced or went into reverse as investors either slowed their buying or fled for the safety of cash. The resulting reduction in assets under management brought a significant hit to revenue. Nevertheless, with more of the pain focused on outflows from index funds, whose fees are lower, there is a trace of silver in the lining for active fund houses.”