Investors were in a much more positive mood in November, according to the latest Fund Flow Index from Calastone, the largest global funds network. But they were very selective.

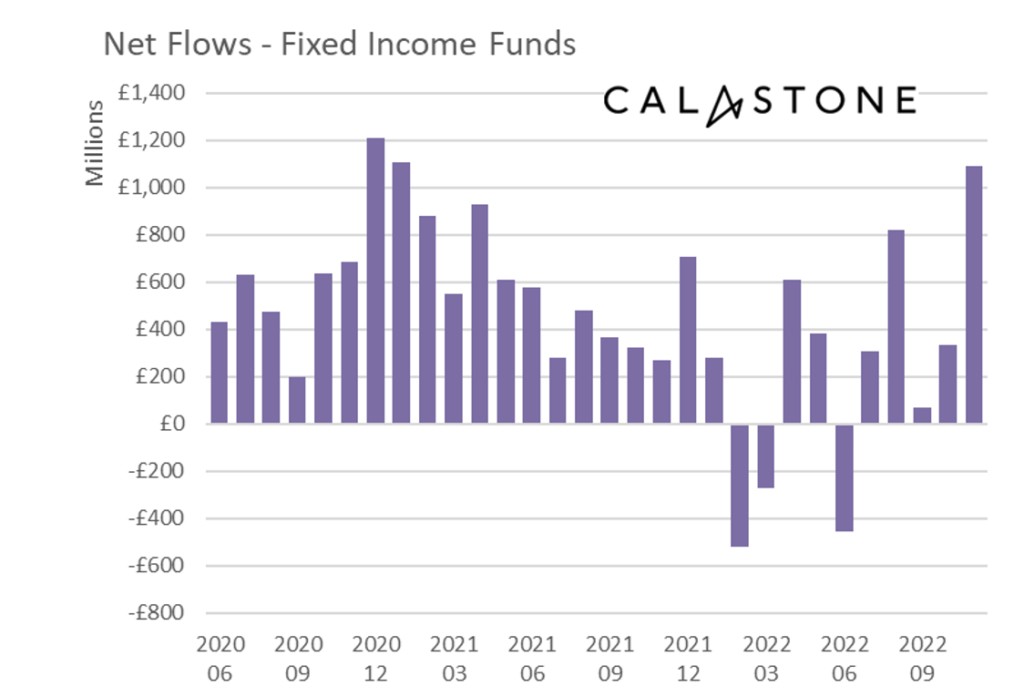

Fixed income funds saw inflows of £1.09bn – the most significant in two years and fourth largest on record

The biggest move came in fixed income. Investors bought a net £1.09bn of bond funds, two thirds of which was undertaken during the first nine trading days of the month. The inflow of new cash was the most significant in two years and the fourth largest on Calastone’s record. It reflected November’s very big fall in bond yields around the world, including in the UK, that accompanied much more benign inflation data than expected in the US.

Edward Glyn, head of global markets at Calastone said: “Any inkling that inflation might be coming under control is good for bond prices because it means interest rates can peak at a lower level. Bond yields are simply market interest rates and when they fall, bond prices move mechanically higher. Investors scrambled to lock purchases in at higher yields in November, securing that superior income on their capital and anticipating capital gains as yields fell and bond prices rose.”

Stock markets followed bond rally – equity funds saw first inflow in seven months

The fall in bond yields sparked a rally in equity markets and equity funds enjoyed net inflows for the first time since April a result. Investors added a net £383m – but there was very wide divergence.

ESG equity funds saw record inflows, and supported flows of capital into global and North American funds

ESG funds had their best month on record after a distinct lull between March and September – investors added a net £1.56bn to their holdings. Global funds also did very well with a £1.02bn inflow, just over half of which was ESG cash. North American equities saw their first inflows since June, also boosted by ESG, while emerging markets had their best month since April thanks to the weaker US dollar.

Asia-Pacific saw fund outflows slow, while Europe remained out of favour

Elsewhere, outflows from Asia-Pacific equities slowed but European equities continued to suffer significant selling (-£238m in November or £2.32bn year-to-date), reflecting the ongoing energy crunch and looming recession across the region.

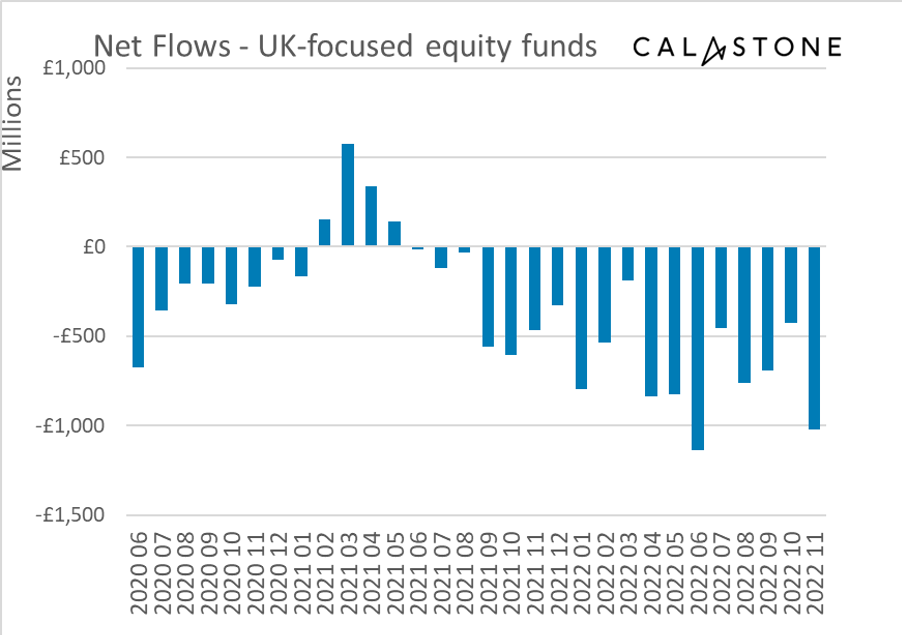

UK-focused funds hit hardest of all – second-worst outflows on record as investors shun ailing UK economy

The UK was worst hit as investor confidence tanked. Outflows surged to £1.02bn in November, the second-worst month on record after June 2022. This was despite a rally in the UK bond market and its associated rise in the stock market. Over the last 18 consecutive months of outflows, investors have withdrawn £9.80bn from funds investing in UK equities.

Edward Glyn explained: “The trajectory of US interest rates is today’s key driver of global markets, but local factors overlay this core factor. In the UK, bond yields rose much higher during the ill-fated Truss interval than among similar nations, but have since come back into line. Fears over the potential duration of the UK’s recession rather than hopes for inflation abating are dominating investor concerns for UK assets. Inflation will fall in the UK in 2023 simply as the anniversary of its acceleration kicks in, but it is becoming entrenched in expectations which will make it harder to eliminate quickly – inflation combined with recession is especially pernicious.

“The worst economic outlook in the G7 helps explain why UK equities are so unloved. Despite low valuations, you can barely give them away at the moment – symbolised by the loss of London’s crown as Europe’s largest bourse. The new Chancellor may have steadied the ship, but there is still not much market confidence yet in the UK economy. The result is an intensification of investor selling of UK-focused equity funds with no end in sight.”