The global ETF market has experienced remarkable growth, with assets under management (AUM) increasing from $11.63 trillion at the end of 2023 to $12.71 trillion in April 2024. Notably, Asia’s ETF market is outpacing global growth, with a 10-year compound annual growth rate (CAGR) of 23.6%, significantly above the worldwide average of 17.5%[1]. To gain deeper insights into the ETF primary market and the factors driving this expansion, we collaborated with ETF Stream to conduct a comprehensive survey, engaging key stakeholders in the ecosystem, including asset servicers, authorised participants (APs), and fund issuers.

While the full report covers global trends, our focus is on Asia, where unique challenges and opportunities emerge for those involved in servicing, distributing, and manufacturing ETFs in Asia. This deeper exploration of the Asian market highlights its distinctive dynamics and reveals critical insights for industry participants looking to navigate this rapidly evolving landscape.

A diverse and growing market

Asia’s ETF market is young compared to the US and Europe, but it’s growing and maturing quickly. Hong Kong, Singapore, and Japan lead the region in ETF activity, and smaller markets like Taiwan, South Korea, and Vietnam are seeing strong growth, largely driven by retail investors. The transportability of UCITS structure has also allowed managers from across Europe and the US to expand their ETF offerings into Asia, cross-listing products into regional exchanges.

However, Asia’s primary market processes are still highly manual and inefficient compared to its global counterparts, and have yet to catch up with the level of efficiency seen within the secondary market. Though this is likely to change very quickly, the relatively low trading volumes and fragmented nature of the region’s markets have delayed the widespread adoption of automation.

Unlike Europe, where ETFs generally operate uniformly across countries, Asia presents a patchwork of processes, regulatory environments and market structures, each requiring tailored solutions. Each country has developed its own systems, resulting in a lack of standardisation across the board, which complicates operations for APs and issuers who need to navigate multiple portals and systems required to operate in different markets.

The technology challenge

As Asia’s ETF market grows, in terms of volumes, the number of products and the complexity of products, so too does the complexity of its servicing needs.

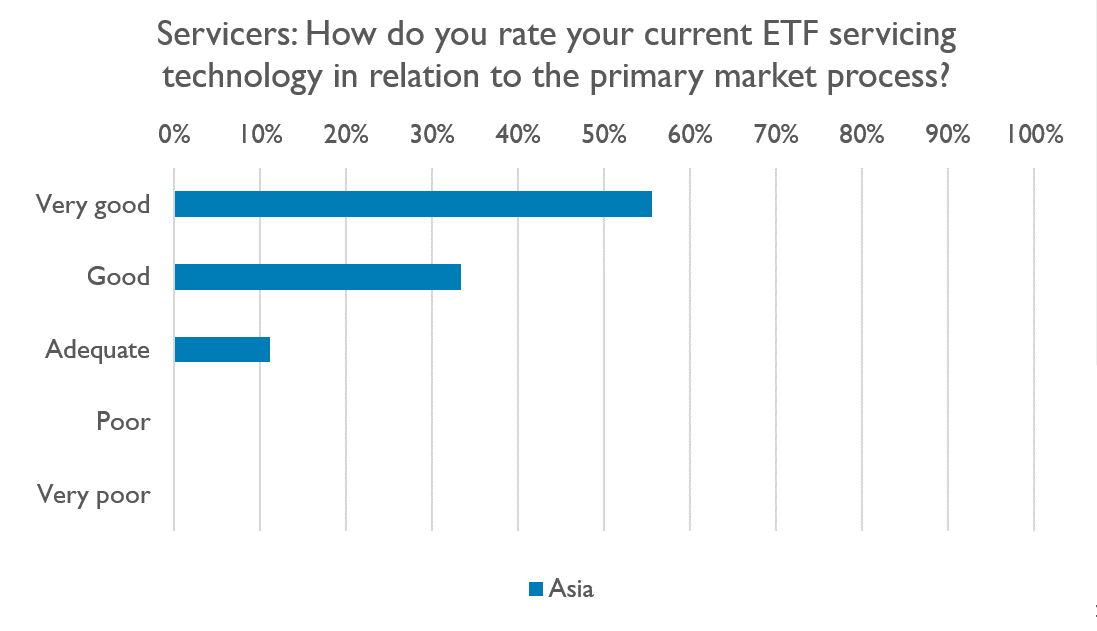

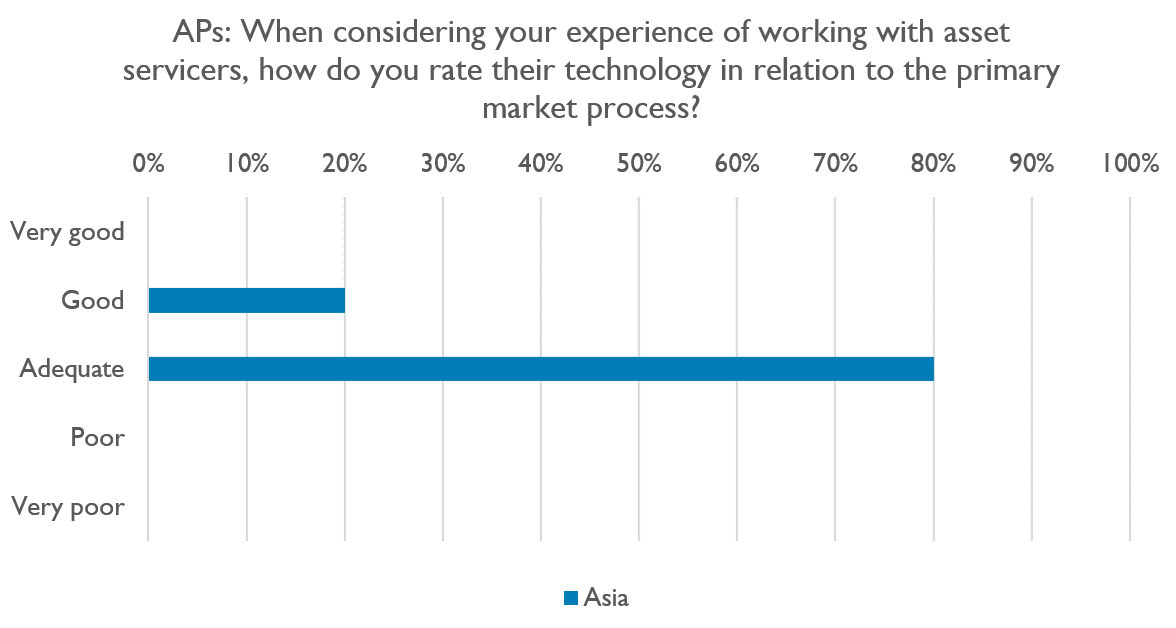

Asset servicers operating in Asia are generally optimistic about the state of their technology, with 57% rating it “very good”. APs and issuers, however, are much more cynical compared to servicers operating in the region. 80% of APs, for example, rated their servicing technology as only “adequate”. This disparity between servicers and the rest of the ecosystem mirrors what we found in the global report.

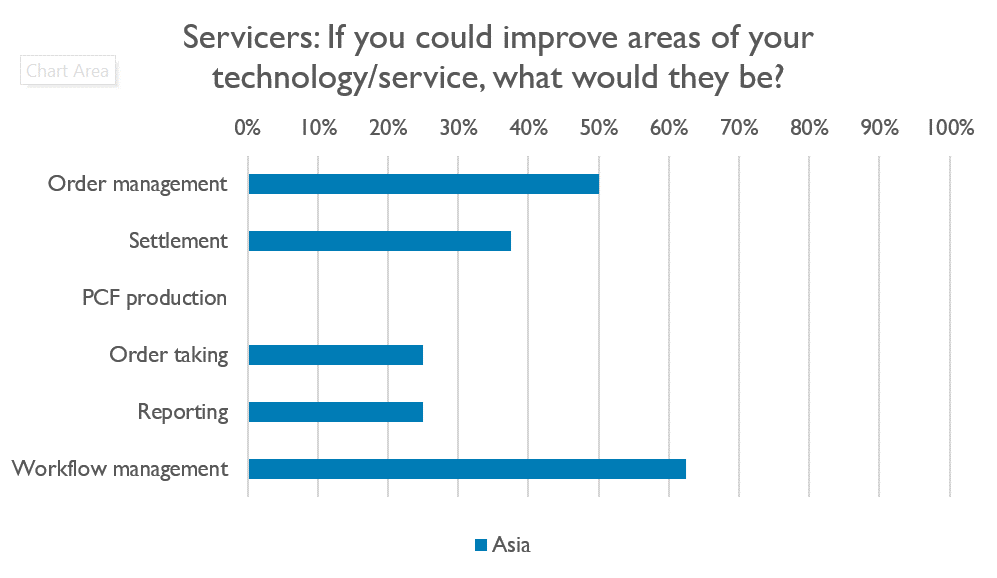

Despite this there is acknowledgement from Servicers that there is much room for improvement, despite their overall optimism, with Servicers operating in Asia identifying workflow management, order management and settlement as key areas for improvement.

Adapting to change

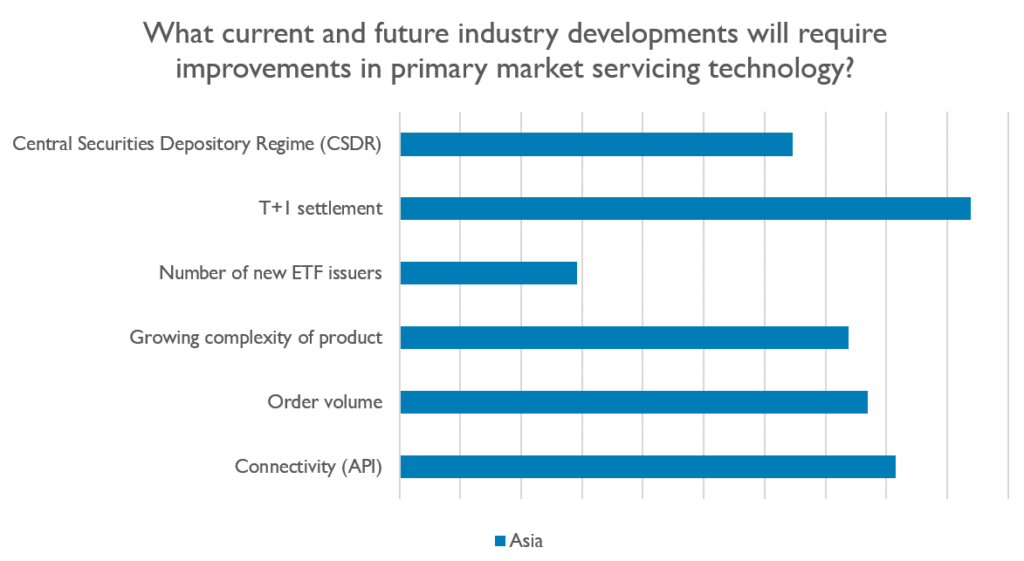

Concerns about the future of the industry revolve around the increasing scale and sophistication of the ETF market – and the ability of technology to keep up. In Asia, the shift to T+1 settlement is viewed as the most pressing development, requiring significant upgrades in primary market servicing technology. While the respondents were generally less worried about new ETF issuer entrants, they are more concerned about order volumes going up. Given the fragmentary nature of the region, and that many processes remain manual, this concern is understandable. The transition to T+1 settlement presents specific challenges in Asia, where you would effectively have to pre-fund transactions 24-48 hours in advance – a task that becomes significantly harder without the right systems and connectivity in place.

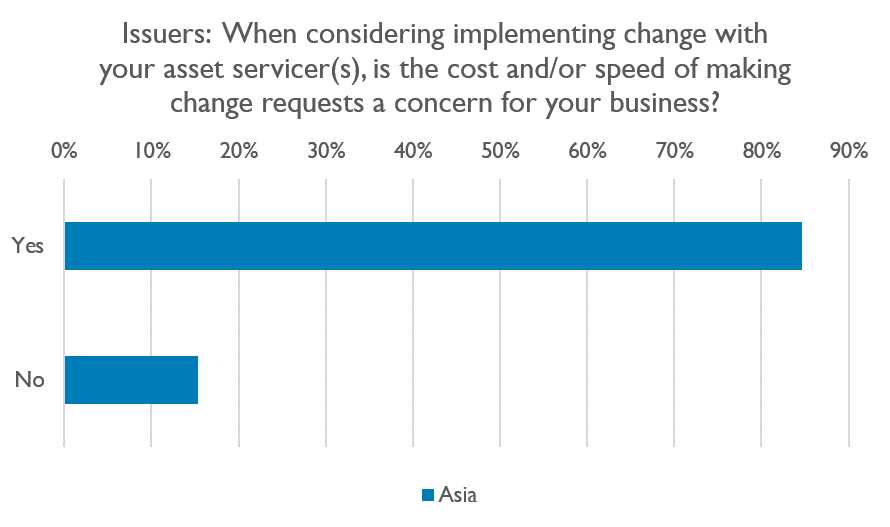

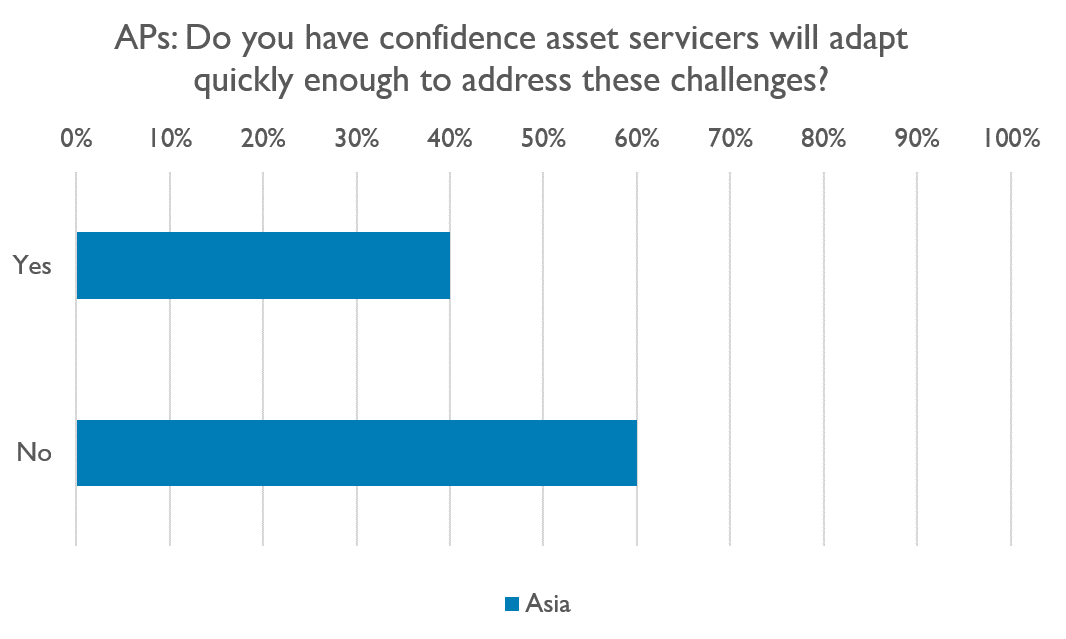

There are varied opinions about how well servicers are prepared to address the challenges needed to implement these future developments. One of the key concerns of fund issuers operating across Asia is the cost and speed of implementing changes within asset servicers. Issuers operating in Asia are relatively optimistic about their servicers’ adaptability, with the majority expressing confidence in their ability to address challenges. However, APs are more sceptical. Across Asia, 60% of APs reported a lack of confidence in servicers’ adaptability to change.

Optimistic outlook

Despite the recognition of the challenges in the Asian ETF market, there is a sense of optimism.

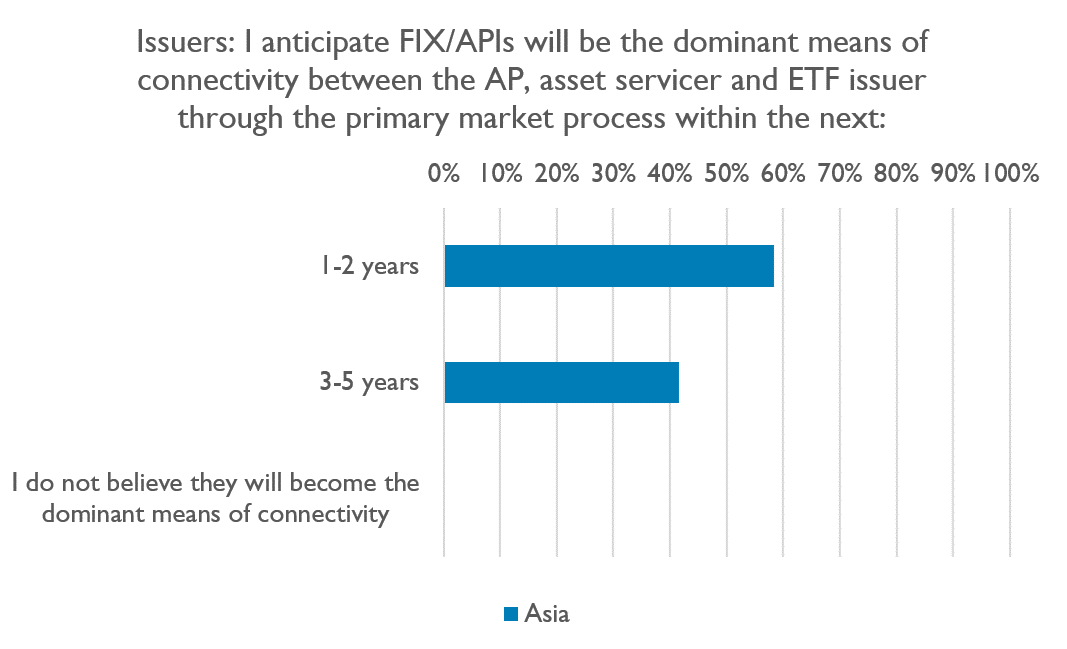

In Asia, there is a strong expectation that FIX and API-based connectivity will become the dominant mode of communication between APs, servicers, and issuers in the primary market, with many predicting widespread adoption within the next one to two years.

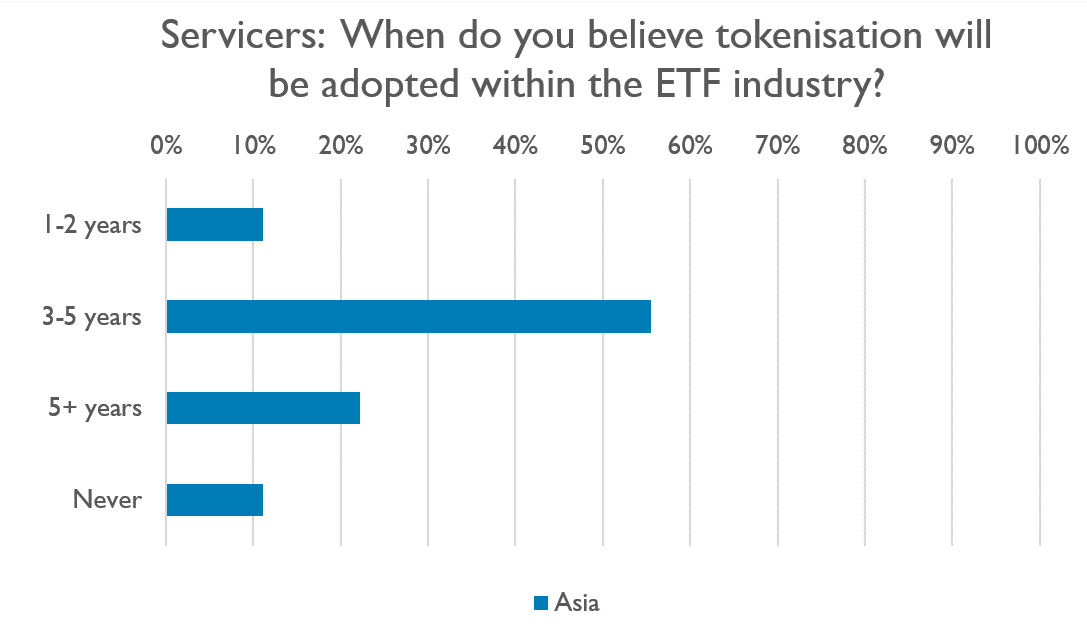

Those operating in Asia also stand out in their attitude toward tokenisation. Two-thirds of asset servicers in Asia believe that tokenisation will be adopted within the ETF industry in the next 1-5 years. That said, issuers and APs are less optimistic, with issuers predicting it will take around 3-5+ years on average. 40% of APs say it will never take hold.

The road ahead

The ETF market in Asia is growing, and fast. Issuers and APs operating in the region are navigating a complex landscape, where regulatory environments and servicing requirements vary significantly from one country to the next. This heterogeneity presents both challenges and opportunities for service providers, who must adapt their technology and processes to meet the specific needs of each market. The primary market in Asia is poised for transformation. Players in the region are more open about the need for improvement, but are also largely more optimistic for the future – and with the right technology, they should be.

Calastone is well positioned to support this growth, and meet the demand for an automated, standardised primary market and replicate the cross-market connectivity we provide to mutual funds within the ETF ecosystem. Working closely with industry leaders and leveraging our partnership with HSBC, we are developing solutions that not only address the current state of the market but also prepare issuers and servicers for the future. As the ETF market in Asia continues to mature and shift towards greater sophistication – moving from in specie and NAV+ creation to more advanced actual cash mechanisms – the complexity of primary market processes will vary across countries. Our technology is designed to support this spectrum of sophistication, ensuring our clients have the tools they need, no matter where they are in their journey toward a more efficient and connected ETF market.

[1] https://etfgi.com/news/press-releases/2024/08/etfgi-reports-assets-invested-etfs-industry-asia-pacific-ex-japan