The growth of decentralised finance (DeFi) has been one of the financial stories of the decade. Total value locked on blockchain – that is, the dollar amount of assets staked on blockchains or related applications – peaked at $237bn last year, up from a few hundred million in 2020. Stablecoin transaction volumes hit $33tn in 2025, exceeding the combined throughput of Visa and Mastercard. Tether, the largest stablecoin issuer, now holds more US Treasury bills ($141bn) than Germany, the UAE, and Australia.

With that scale has come a familiar corporate problem: how to manage a large balance sheet. DeFi treasuries want what any treasury wants – safety, liquidity, and yield – but most are still relying on traditional money market funds or bank deposits to get it. The opportunity for asset managers to serve that demand is clear, and in doing so to reach untapped investor cohorts in the DeFi space, an entirely new pipeline of customer acquisition. But to connect with this market they must first become compatible with it, offering products that can be traded and held on blockchain – tokenised versions of their traditional funds.

To understand how the industry is approaching this, last year we commissioned ValueExchange to survey 52 asset managers and seven DeFi/Web3 platforms on the state of tokenised fund distribution. We wanted to know how asset managers are approaching the opportunity, which products they are bringing to market first, which distribution partners they favour, and where the practical barriers lie, and we wanted to test the demand side, examining how DeFi platforms think about tokenised funds and what they expect them to unlock.

In this paper, we look at what the research tells us about the global picture, and then zoom in on Asia-Pacific, where the shape of the opportunity, and the barriers to realising it, differ.

While demand from DeFi platforms is a key driver of this shift, the same distribution model is also being adopted across regulated digital platforms and wealth channels, particularly in Asia’s leading financial centres.

The immediate opportunity for asset managers is in the distribution of tokenised funds. Rather than undertaking end-to-end tokenisation, which would involve digitising the entire value chain, asset managers are tokenising only the fund unit, leaving the underlying structure intact. This allows them to reach new investor cohorts quickly, often without creating new share classes, and with minimal changes to existing infrastructure.

Most asset managers are already putting tokenisation into practice. According to our research, almost three quarters have reached the point where they have at least put a tokenised project in motion, and among those who have already launched a tokenised fund, 65% report that the experience offers benefits over the traditional model, with access to new customers and automation among the most commonly cited advantages.

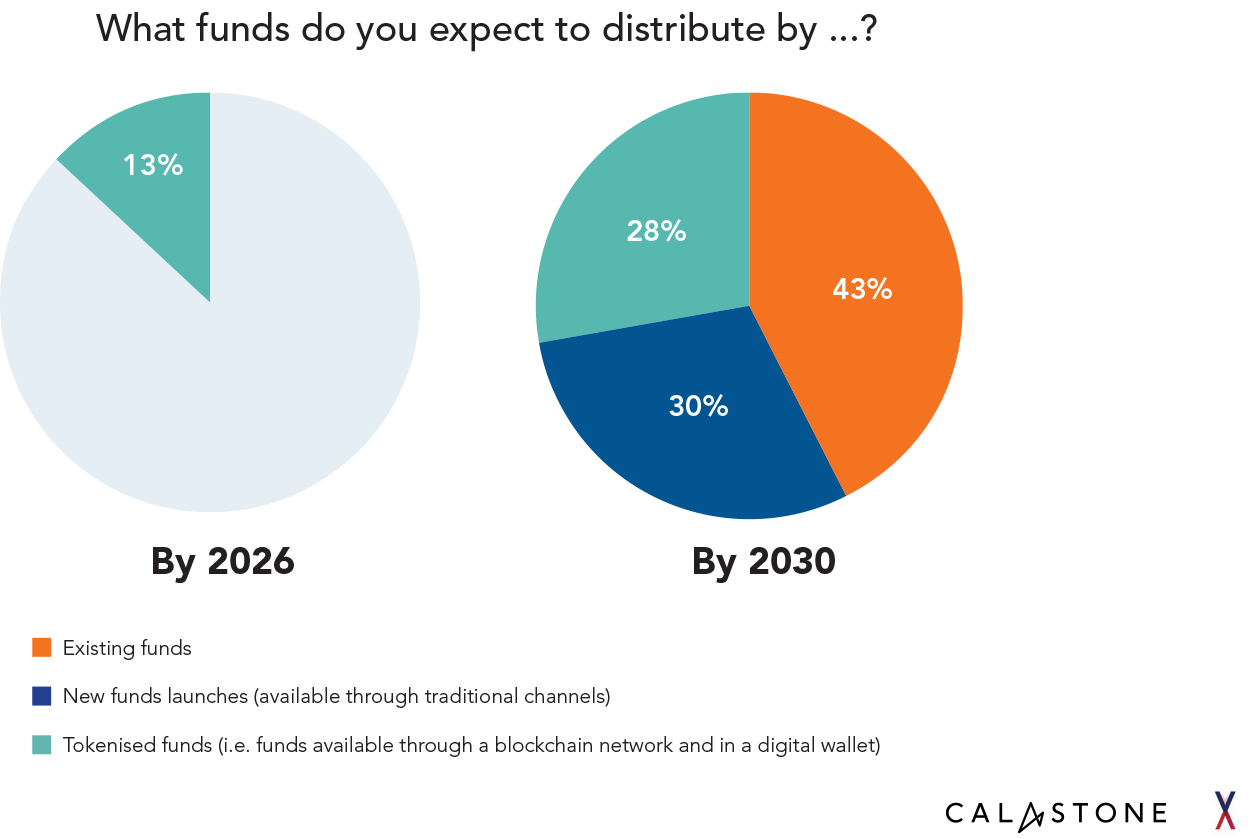

The share of asset managers distributing tokenised funds is set to reach 13% this year and 28% by 2030. Our research projects the AUM of tokenised funds will grow from $4bn in 2024 to $235bn by 2029, a 58x increase. Other estimates have been even more bullish: a PwC report earlier this year projects $715bn by 2030. Tokenised money market fund AUM alone grew from $4bn at the start of 2025 to $8.6bn by November, up 110% in under a year.

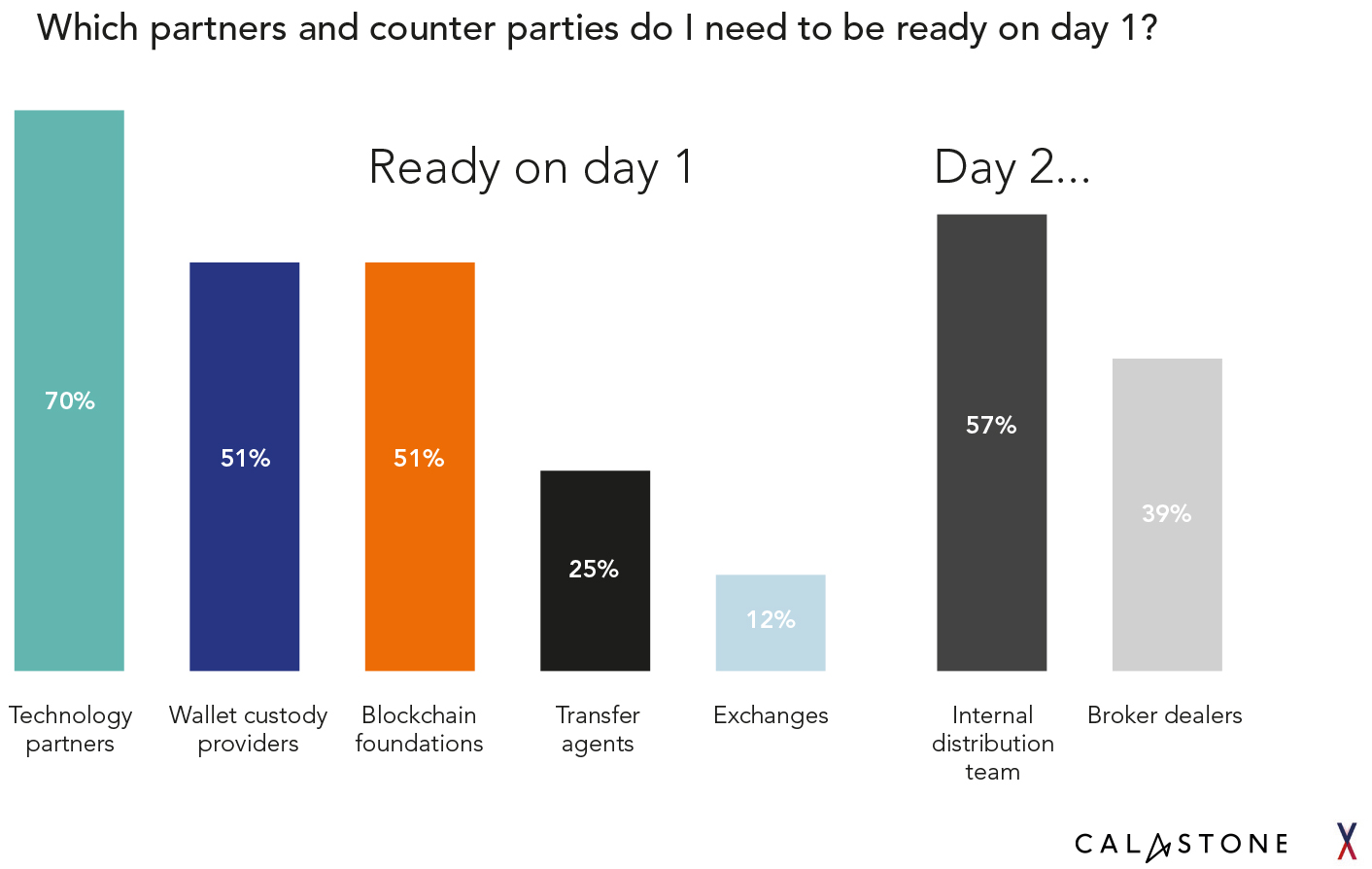

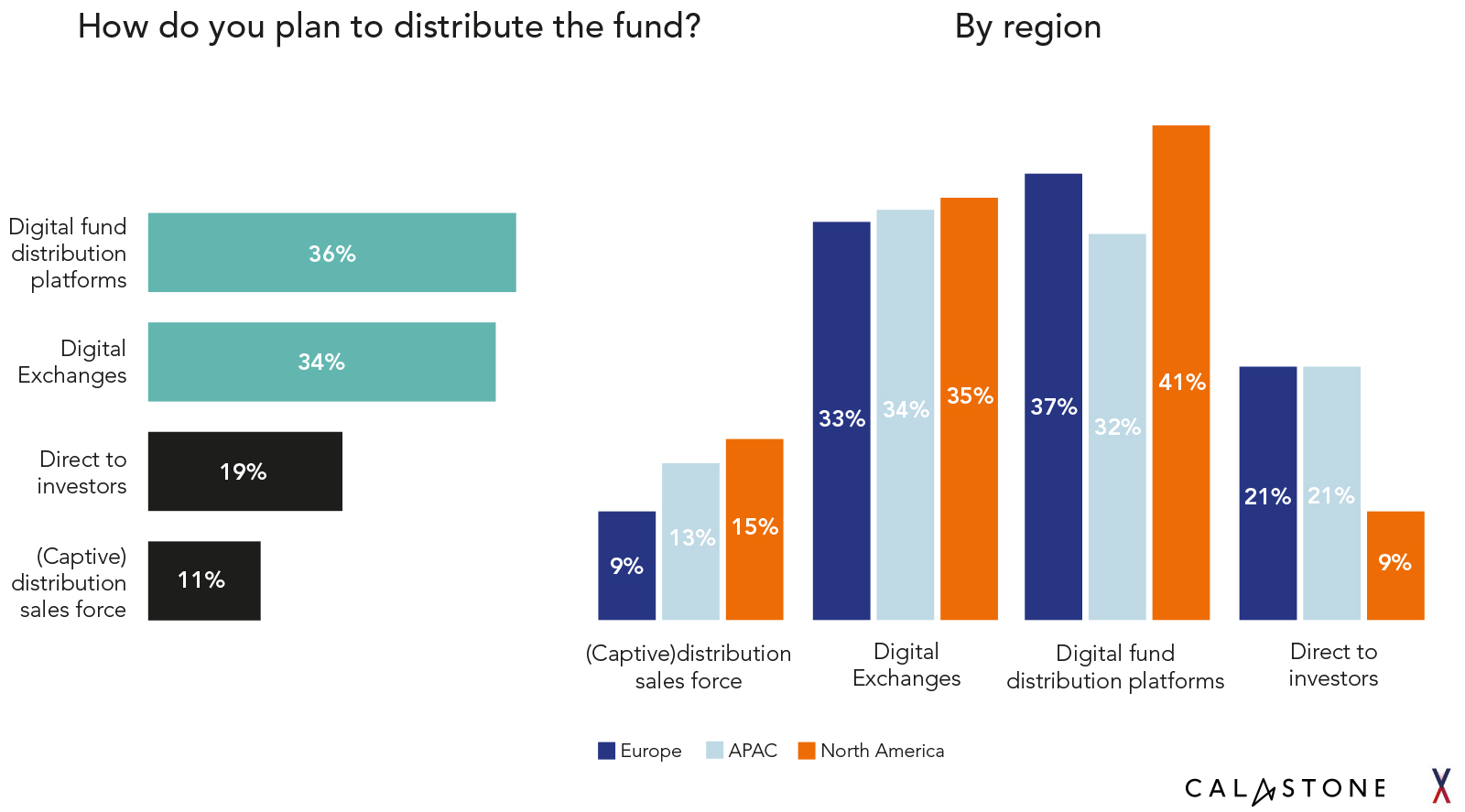

To get there, asset managers are converging on a similar approach. They are prioritising working with third-parties to facilitate distribution of tokenised funds. Asked what resources they wanted in place as a Day 1 priority, the most popular response – identified by 70% – was technology partners. The same share of respondents said they plan to distribute through intermediaries, with 36% preferring digital fund distribution platforms and 34% digital exchanges.

In contrast, just 19% said they would go direct to investors and 11% that they intended to rely on a captive distribution sales force. Rather than making extensive investments into internal resources and capabilities, there is a desire to lean on third parties when it comes to the distribution of tokenised funds, with an emphasis on getting to market quickly and leveraging partners already active in the market.

By focusing on a digital distribution model, asset managers are also hoping to overcome some of the issues of the traditional model, such as slow and costly onboarding, the challenge of regional regulatory variation and limited data transparency. Digital intermediaries that are already accustomed to working across different territories can help to ensure speed to market, as well as facilitating greater transparency for customers and personalised investor journeys.

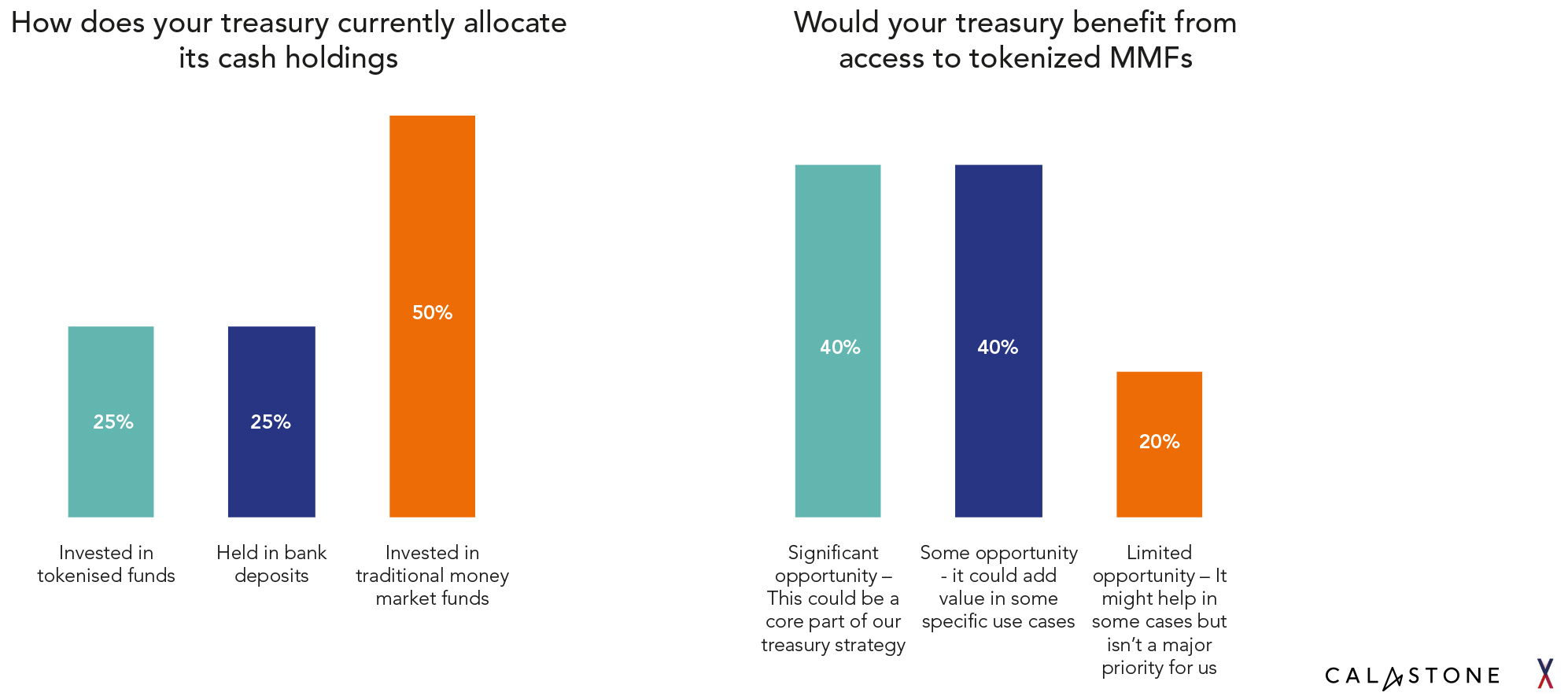

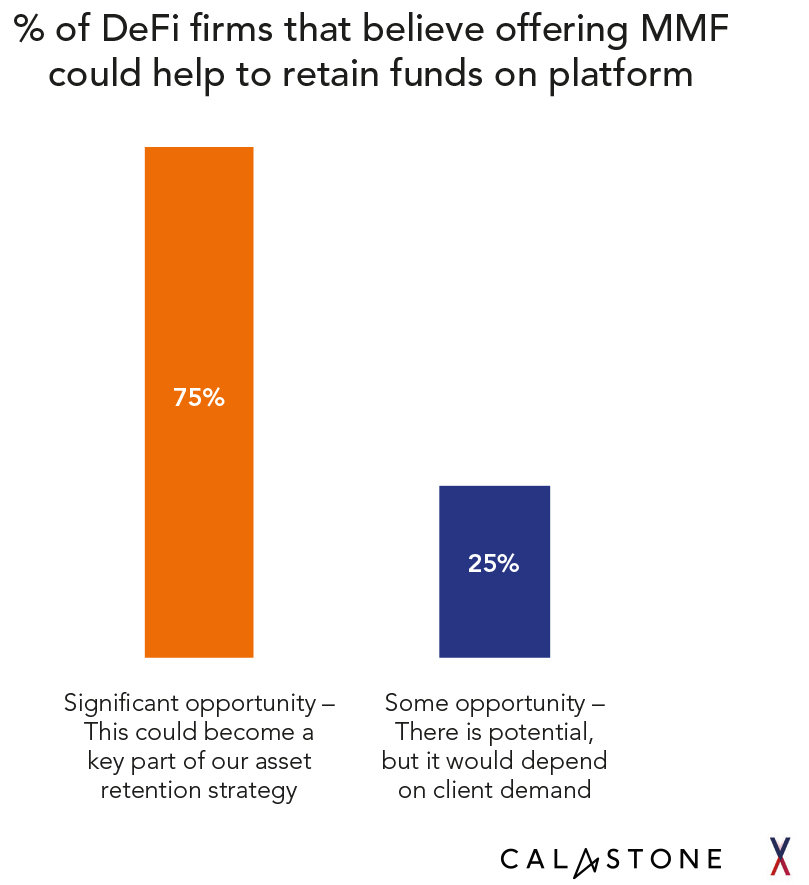

On products, MMFs and private asset funds are the most favoured for tokenised distribution. MMFs have a particularly strong fit with DeFi demand, because they combine the core features of a traditional cash product – low risk, liquid, yield-bearing – with the additional benefits of direct integration with digital wallets, improved transparency, and the ability to purchase using stablecoins. This is already seeing institutional use. BlackRock’s BUIDL fund is now accepted as collateral for institutional trading on Binance, and J.P. Morgan launched an intraday repo solution using tokenised collateral that reached $1bn in daily trading volume in its first month. Among the DeFi platforms we surveyed, eight out of ten said tokenised MMFs could benefit how their treasuries manage assets and three-quarters saw them as a tool for client retention. Within five years, half expect to have increased their tokenised holdings by at least 25%.

While MMFs are emerging as the clearest near-term use case, they are unlikely to be the end state. Private markets, which ranked equally highly in our research, offer a complementary opportunity, particularly as tokenisation begins to address long-standing challenges around access, liquidity and transparency in less accessible asset classes.

More broadly, this points to a wider shift. Treasury management is the entry point, but not the limit of the opportunity. As DeFi platforms evolve beyond balance sheet management into full-service financial ecosystems, tokenised funds provide a way to expand their product offering to end investors — effectively creating a new digital distribution channel for traditional asset managers.

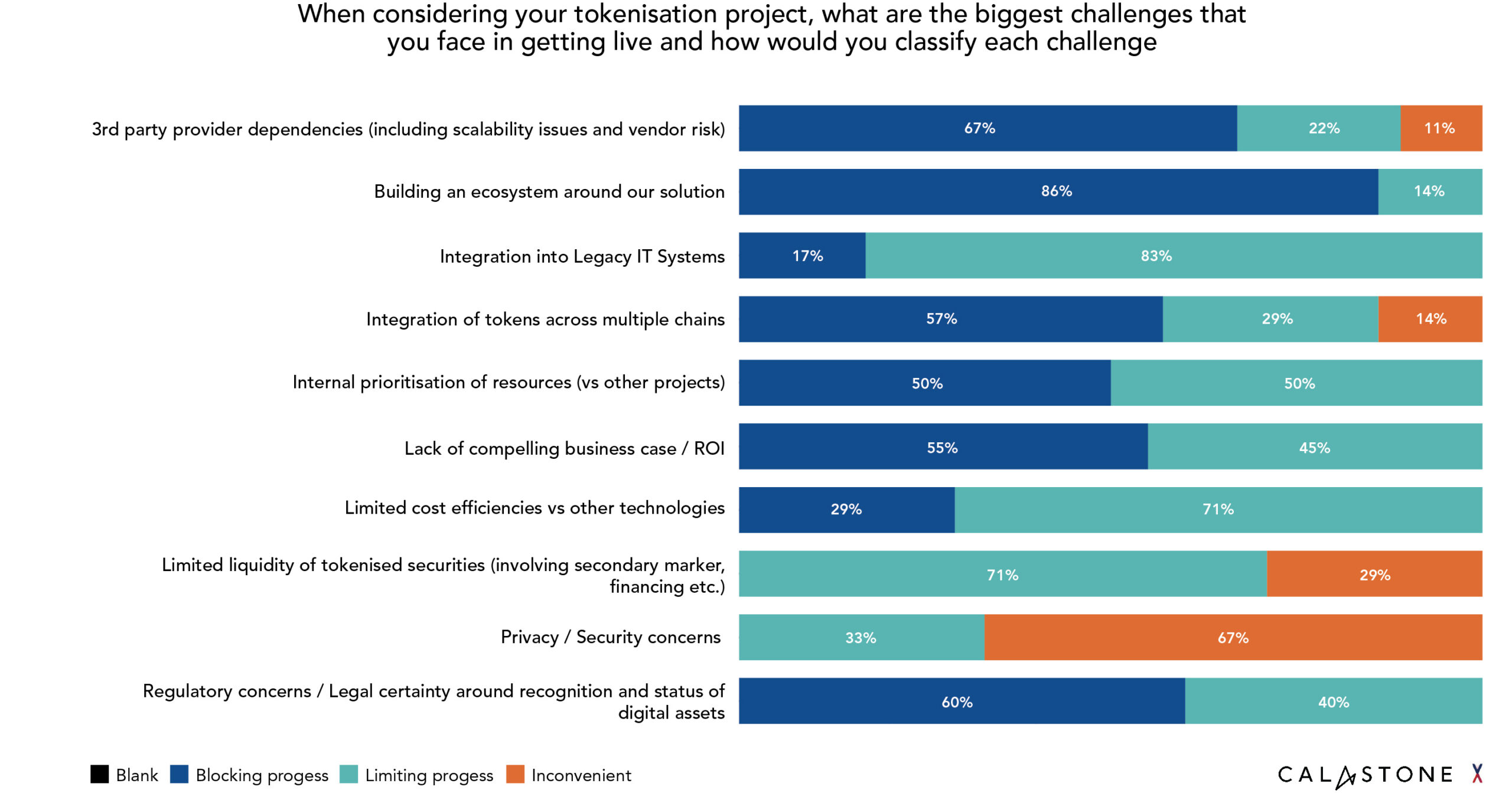

Two years ago, our research suggested that Asian asset managers were leading the global charge on tokenisation, with 86% expecting to offer tokenised funds within three years. That specific timeline has proved ambitious, but the direction of travel has held. What has changed is where the barriers now sit. The question is no longer whether product will be available; it is whether the operational and ecosystem conditions exist for distribution to work at scale. So, while APAC broadly aligns with the global consensus on approach, there are some interesting differences in where the barriers lie. This is playing out against a backdrop of rapid regulatory development across the region, with markets such as Hong Kong and Singapore actively shaping the frameworks for digital asset distribution.

The vast majority of global respondents said that the lack of a compelling business case or ROI was either blocking their progress (44%) or limiting it (41%). The single largest blocker for APAC, however, is the challenge of building an ecosystem around tokenised solutions. Some 86% of respondents in APAC said that building an ecosystem around their solution was blocking progress, compared to a global average of 34%. At the same time, certain traditional constraints appear less acute. Integration with legacy systems is less likely to be seen as a hard blocker, and privacy and security concerns are not elevated to the same extent as in other regions.

Closely related is a second area where APAC stands out: integration across blockchain networks. Firms in the region are significantly more likely to see interoperability across chains as a blocking issue (57%) than their counterparts in Europe or North America (28%).

Taken together, these findings point to a more advanced stage of thinking. Unlike traditional fund models, which can operate within established distribution networks, tokenised funds rely on a broader and less mature ecosystem. The primary challenge in Asia is not building a product, but ensuring that product can operate within a fragmented and still-evolving ecosystem. While MMFs are a natural starting point given their fit with on-chain treasury use cases, the broader opportunity in Asia is not limited to liquidity products. As digital platforms in the region evolve, the ability to distribute a wider range of traditional assets on-chain is likely to become increasingly important.

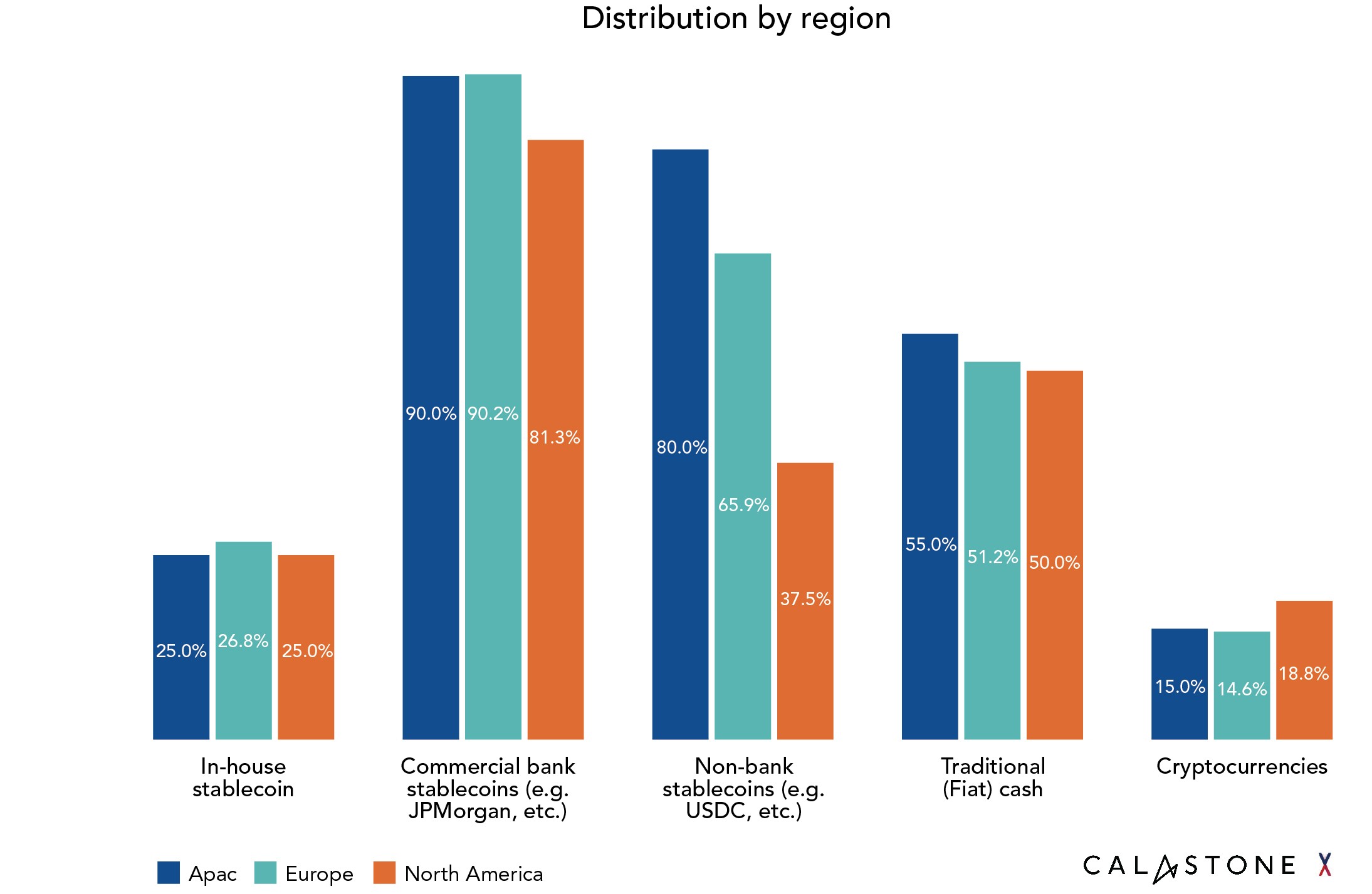

A third point of differentiation is that firms in the region are notably more open to non-bank stablecoins than their counterparts in Europe and North America. Bank-issued stablecoins are widely accepted everywhere, but APAC shows a greater willingness to incorporate a broader range of blockchain-native payment mechanisms alongside them. At the same time, the region maintains strong acceptance of traditional fiat, suggesting an expansion of settlement options rather than a shift away from existing ones.

This points to three requirements for making tokenised distribution work in the region.

First, asset managers should plug into existing ecosystems rather than attempting to build their own. In Asia, where the ecosystem challenge is most acute, the case for working through established networks is even stronger. A platform such as Calastone’s, which already connects asset managers, distributors and service providers across the region, offers a distribution layer that minimises the need for new connections and avoids the fragmentation risk of parallel digital and traditional ecosystems.

Second, design for interoperability from the outset. With multiple blockchains in use across the region’s markets and platforms, the ability to distribute across chains is a requirement for scale.

Third, support multiple payment rails. Fiat, bank-issued stablecoins and non-bank stablecoins each have a role to play in meeting the varied preferences of investors and platforms across the region. APAC’s openness to this range is a competitive advantage, if the infrastructure supports it.

Volumes remain modest, and the region faces operational challenges in ecosystem coordination and blockchain fragmentation, but this is being met with a growing pipeline of live products and regulatory progress in emerging markets.

The last year has seen a succession of product launches across Asia. HSBC and Standard Chartered have both been granted stablecoin licences by Hong Kong as they bring tokenised products to market in the region. Thailand’s Securities and Exchange Commission recently amended its regulations to accommodate the sale and redemption of tokenised mutual funds, joining Singapore and Hong Kong as jurisdictions actively enabling digital fund distribution. Markets that, only recently, would not have featured in the tokenisation conversation are now positioning themselves alongside the region’s established financial centres.

Globally, the direction of travel is the same. Legal & General has announced that its liquidity funds, representing over £50bn in assets, are now live on Calastone’s Tokenised Distribution Network, bringing a major global asset manager onto blockchain-enabled distribution infrastructure in a live production environment. Liquidity funds are a natural starting point, combining capital preservation, same-day settlement and competitive yield within a structure investors already understand. The launch is a tangible sign that tokenised distribution is moving from theory into practice.

Asia’s tokenisation journey has been slower than once predicted, but also more deliberate. Compared to the rest of the world, the region has a different hierarchy of issues – one that reflects a shift away from internal readiness and towards external dependencies. Yet the ecosystem challenge is not one that asset managers need to solve alone. Those that work through established networks and distribution platforms, rather than building from scratch, will be best positioned to move quickly.