This paper sets out the practical and economic implications of tokenisation in asset management. It evaluates the cost structure of the industry, breaking down the operating expenses of an average fund, the savings and revenue improvements that could be achieved through tokenisation, and the economic impact of tokenisation on the industry as a whole.

It is supported by an in-depth survey of 26 asset managers, which found:

The survey, conducted with research partner ValueExchange, sourced fund-level data from 26 asset managers. It benchmarked the costs of setting up and operating a traditional fund, and worked with them to calculate the differences of using a tokenised approach to launch and run funds. It found a range of expectations about the tokenised future for asset management: while the average projections showed considerable improvements in cost efficiency and profitability, some respondents expected even more dramatic improvements in launch timelines, cost reduction and revenue growth.

In its final section, the paper looks at how asset managers are working towards the opportunities of tokenisation, as well as their concerns: among those not yet using DLT, 55% cited worries about deployment costs, and 30% said that feature-based limits of the technology and an unclear business case are the biggest obstacles to realising the benefits of tokenisation.

Calastone’s view is that tokenisation will become a core pillar of strategy for most asset managers, but that the journey to that end state is likely to be incremental and require a phased approach. This paper sets out some of the steps involved, and estimates the value asset managers can hope to unlock by pursuing them.

Introduction

Tokenisation is rapidly gaining ground across asset management. The conversion of assets into digital tokens that are held on distributed ledgers will be not just a technical upgrade but a wide-reaching transformation for the industry.

For asset managers, tokenisation promises to make funds quicker to launch, easier to distribute and less expensive to manage, cutting through the operational inertia that creates a heavy burden of time lost, costs incurred and errors committed. It is an opportunity the industry appears eager to grasp, mirroring previous cycles of major technological change.

But how quickly, effectively and comprehensively will the potential of tokenisation be realised? And what will it mean for the business model and cost structure of asset management?

This research has sought to answer those questions, providing a comprehensive economic evaluation of tokenisation in the manufacturing and administration of funds. Based on a detailed survey of asset managers, it breaks down the current cost lines they face, the rate at which those are currently growing, and the extent to which tokenisation is expected to deliver cost savings, wider efficiency benefits and growth opportunities.

In place of broad predictions and long-term projections, it seeks to define in concrete terms how much value tokenisation will add to asset management, for both the industry as a whole and for the typical business. It isolates where cost pressures are being felt most acutely, identifies the areas where tokenisation can make a difference, and illustrates how it can provide a catalyst for future growth.

Above all, it brings the issue of tokenisation down to the level of the individual fund. If a mutual fund or ETF is built, operated and distributed on blockchain as a tokenised entity, how much more quickly and cost-efficiently can it be launched? How much cheaper will it be to run? What will the knock-on effect be on the manager’s ability to distribute that fund and reach a wider base of investors?

As asset managers begin to pilot tokenised funds in various forms, these are increasingly the questions that they need to answer. And they are becoming pressing as the costs of running traditional funds and ETFs continue to climb – a challenge amply demonstrated by this research.

Through surveying a representative group of managers overseeing US (40 Act), UK, UCITS and VCC funds, this research has sought to provide the best estimate yet of what results managers can expect from tokenisation, and where in their business models they may realise the greatest benefits.

The headline findings are that the impact of tokenisation should be transformative for the business model of asset management. Cost savings in the order of 23% are projected, with resultant scope to make significant fee reductions and attract more investors. Across major fund types, there is an estimated $135.3bn benefit to overall P&L. These figures are based on the current expectations of asset managers, which themselves cover a spectrum of more and less bullish projections. The ultimate impact of tokenisation, as the underlying technology matures and understanding of it grows, may be even greater than what is set out there.

Each asset manager will have their own approach to pursuing tokenisation, and this report also explores some of the different paths to implementation. But the core opportunity of a new technological infrastructure for the industry is one that will affect every participant. Increasingly, we will look at asset management before tokenisation and after tokenisation as different eras for the industry.

This research stakes out how some of that change will happen, where its effects will be felt, and how asset managers can move to take advantage.

For asset managers, the business case for tokenisation is grounded both in future potential and present problems. While this survey found a range of expectations around the benefits of tokenisation, there is little dispute about the collective starting point – a baseline of high and rapidly climbing operating costs. No small part of the appeal of tokenisation is that the status quo is becoming more and more expensive to maintain.

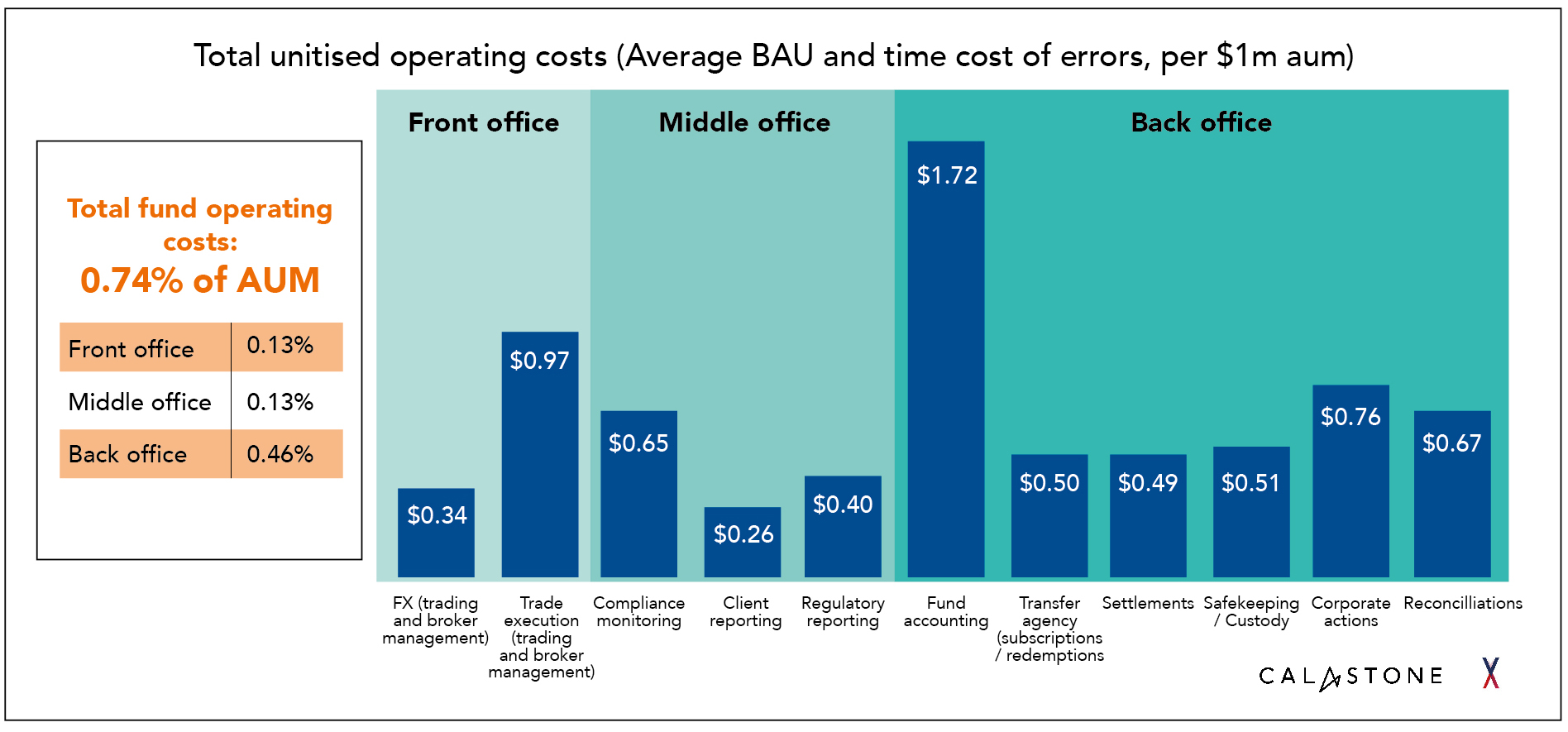

As of 2024, operating costs already amount to 0.74% of AUM for the average fund, with those expenses heavily concentrated in the back office, where fund accounting, corporate actions and reconciliations are three of the four most expensive line items overall (Figure 1). The back office currently accounts for 64% of fund operating costs, and fund accounting alone is responsible for almost 24% of the total. Half of survey respondents said that operating cost pressures are driving a need for change in fund accounting.

Figure 1: Total unitised fund operating costs per $1m AUM

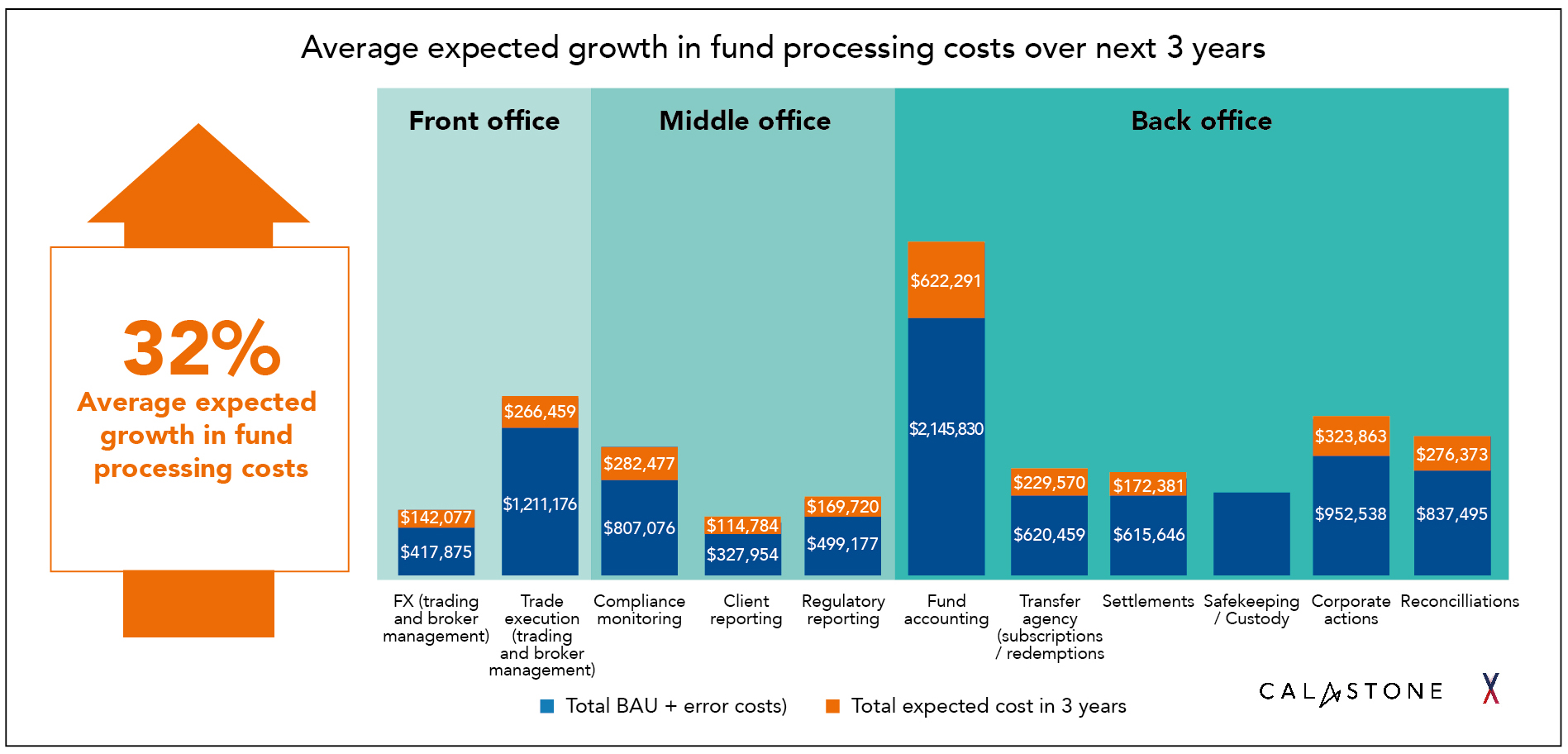

That desire for change is rooted in a recognition that these costs are only going to keep increasing. Over the next three years, asset managers expect fund operating costs to rise by 32% (Figure 2). For the average fund, the costs involved in transfer agency will be 37% higher in 2027 than they were in 2024, client reporting and compliance monitoring will be 35% more expensive, and regulatory reporting will be up by 34%. Of eleven different line items, only one (safekeeping/custody) is not expected to rise in cost over the next three years.

Costs are set to grow across front, middle and back office functions, and among business lines both managed in house and by third parties. Current operating costs are split fairly evenly between internal staff headcount (47%) and third party provider costs (53%).

Asset managers are hurt by rising costs in multiple ways. The survey found that managers are bearing more of the expense themselves (0.4% of AUM) than they hand on to the customer in fees (0.34% as the contribution of operational costs to a total TER of 0.8%). Rising expense levels therefore represent a direct hit to the bottom line.

In turn, as costs rise, it is inevitable that at least some of that increased burden will feed through into higher fees, damaging the competitiveness of funds and their ability to reach a wider audience of investors.

Figure 2: Average expected growth in fund processing costs, 2024-2027

Against this backdrop, the potential of tokenisation to make funds less expensive to launch and run becomes a cornerstone of its strategic value. The second chapter of this report sets out exactly how asset managers expect tokenisation to improve fund operating costs and profitability.

Equally, asset managers have concerns above and beyond the cost of doing business. When asked about the business challenges with the greatest impact on them, 40% said the most important issue was the time it takes to set up a fund, which prevents distribution to new channels, ahead of 33% who identified the cost of establishing a new fund, and how this limits their ability to distribute the fund and provide customisation for smaller investors.

As this suggests, asset managers want to move more quickly and respond with agility to changing customer needs, as much as they feel the need to cut costs. Regulation is also a major concern: 62% of respondents said it is driving the need for change in compliance monitoring, 50% in FX and 45% in trade execution.

The underlying principle of tokenisation – that distributed ledgers and digital tokens make it easier to record, verify and transfer the ownership of assets – supports all of these needs. The technology has attracted so much attention precisely because a tokenised fund, in theory, simplifies or makes redundant many of the processes that have created a complex and costly value chain within asset management. When core tasks such as transferring assets and verifying ownership can be done seamlessly, without error or delay, it becomes easier to launch new products, respond to customer demands and meet additional regulatory requirements.

That is in principle. But how quickly will those benefits be felt in practice? Where in the P&L of an average fund can asset managers expect to see the difference? How significant will the financial impact of tokenisation really be?

Technological trends are notoriously difficult to predict, both in the pace of their adoption and the scale of their impact. While entirely accurate projections may be impossible, honest ones can be found by asking the people working at the coal face, making investment decisions around those technologies. That is why this research focused on a detailed survey of asset managers, going line-by-line through their costs, current and projected.

We worked with them to look into the future. With the benefit of tokenisation, how much cheaper and faster might it become to launch a fund? What would the impact be on running costs? How much more attractive might such funds become to investors, and would there be a consequent benefit to AUM?

Respondents were clear that they expect tokenisation to make a significant difference to the efficiency of fund operations, and that this will be reflected in a boost to the bottom line.

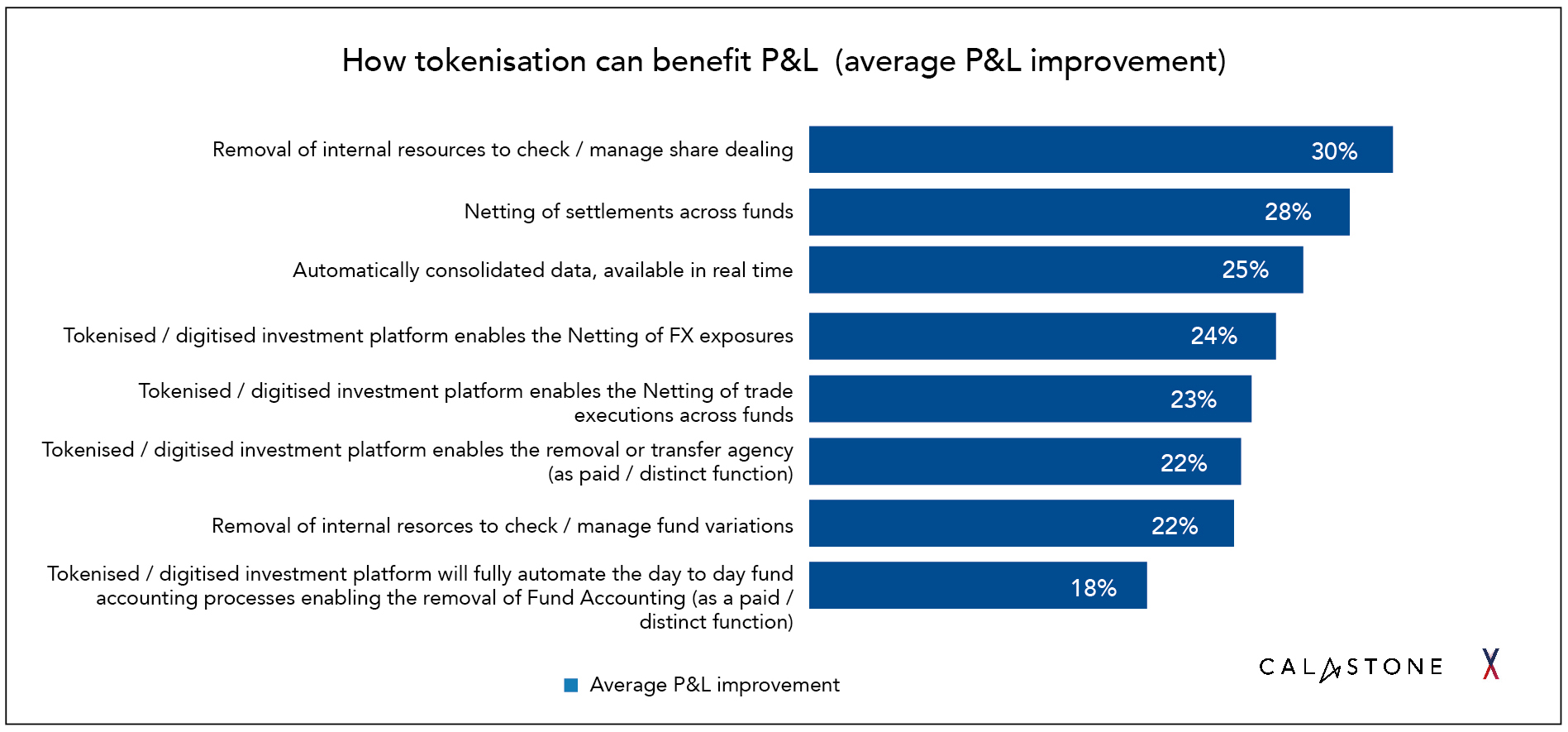

They identified a raft of likely efficiencies (Figure 3), the most financially significant of which were:

Figure 3: How tokenisation can benefit P&L

These improvements highlight the almost devastatingly simple benefit of tokenisation in fund management. By moving funds onto distributed ledgers – which provide a transparent, verifiable, immutable record of ownership, allowing pieces to be moved around without having to perform manual checks and balances – managers circumvent many of the cumbersome processes they currently rely on to keep track.

Rather than data being moved from department to department, switched back and forth between the fund manager and its third party providers, shifted across different systems and sometimes formats, it sits on the ledger. Changes can be made, recorded and reconciled seamlessly. On this basis, the status quo of segregated custody accounts for each fund could eventually give way to large pools of assets covering multiple funds, with DLT ensuring the compliance and clarity over ownership that currently involves numerous manual interventions, each carrying their own cost.

The attractions of these changes are self-evident. The financial implications are also wide-reaching. In the same areas where fund managers are currently experiencing fast-rising costs, they expect tokenisation to deliver substantial savings.

For the average fund, tokenisation is expected to generate a 30% cost saving on fund accounting, a 25% saving on transfer agency costs, and 24% on compliance monitoring, client reporting and regulatory reporting.

Across the board, these improvements are expected to amount to a 23% saving on current costs, or 0.13% of AUM. In dollar terms, the average fund will be saving more on its fund accountancy costs alone than it currently spends on any of the ten other line items.

With lower running costs will come greater flexibility and competitiveness, notably the ability to attract customers through lower fees. In fee-sensitive segments, lower TERs can enhance the attractiveness of funds, leading to increased inflows, higher AUM and ultimately greater revenues from management fees. Lower TERs may also enable funds to penetrate underserved markets, foster investor loyalty and reinvest in distribution and innovation.

For their larger funds (>$10bn AUM), managers expect that a 10% reduction in TER will deliver a corresponding 10% boost in AUM both from wealth investors and retail investors, as well as 6% from institutional investors. In pockets of the market, this growth could be substantial: a majority of respondents (55%) expect the AUM boost from wealth investors in larger funds to be in the order of 11-25%. And some believe the change will be even greater. Almost a fifth (18%) of respondents said that AUM growth from retail investors in larger funds will be north of 25% as a result of tokenisation – hinting at the transformative potential of TER reductions applied to the right customer audiences.

Asset managers, therefore, believe that tokenisation will make funds less expensive in every sense, spurring a virtuous cycle of lower operating costs which can lead to more competitive fees and improved revenue.

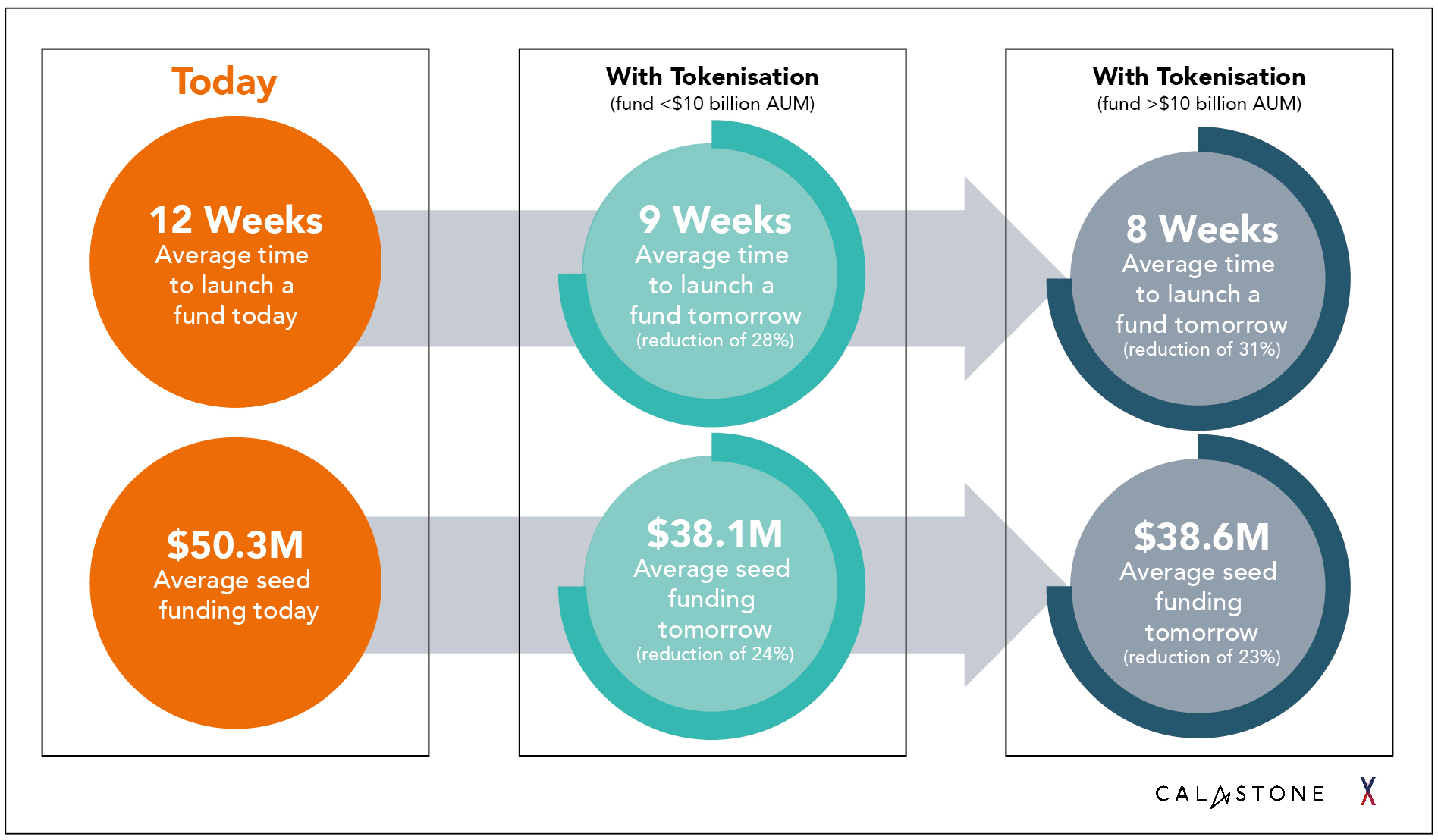

They also expect that tokenisation will allow them to set up funds more quickly and cost-efficiently in the first place (Figure 4). At present, it takes 12 weeks on average to launch a new fund and consumes $50.3m in seed funding. Those figures inflate to 14 weeks and $63.5m when the fund is operating cross border, reflecting the additional work required to work across multiple regulatory systems and set up the necessary infrastructure in different countries.

With tokenisation, the time to launch a fund shrinks to 9 weeks, or 8 weeks for those with more than $10bn AUM (a 28-31% reduction). The cost comes down to $38.1m, or $38.6m for larger funds (23-24% reduction).

Those are average figures, and there are asset managers who believe the improvements will be more substantial: 4% of respondents expect that the time to launch a new fund will decrease by more than half, accelerating the process by at least 6 weeks, while 38% said that they expect seed funding costs to diminish by between 26-50%, suggesting savings of up to $25.2m.

Tokenisation, therefore, is expected to deliver multiple layers of financial advantage to asset managers. It will allow them to launch funds more quickly and less expensively, to operate them more cost efficiently, and to offer more competitive fees to their investors. It promises a future where asset managers can cut costs and boost revenue simultaneously.

Figure 4: The impact of tokenisation on the cost and time to launch of a new fund

In the central case, all these improvements aggregate into a substantial benefit to the bottom line. For a new fund, assuming AUM of $1bn, the overall P&L improvement will be $3.1m (0.31% of AUM) once reduced time to launch, lower seed funding, reduced operating costs and improved revenue from lower TER are taken into account. Taking the assumptions of the most bullish respondents, that P&L improvement would be measured at $7.9m.

Applying the central assumptions to the entire universe of UCITS, UK and US (40 Act) funds suggests that as an industry, asset management can expect to save $135.3bn as a result of tokenisation, a 30% improvement on the current situation.

That is the potential if asset managers can unlock the power of tokenisation to launch and operate their funds more quickly, efficiently and flexibly. Not according to consultants, futurists or economists but to the people who know best and matter most – the managers themselves. And these figures are based on what asset managers estimate today: in reality, the long-term benefits from tokenisation could be even more significant.

The prize on offer is substantial, but no-one in asset management pretends it will be quick or easy to unlock. The next chapter will explore some of the most prevalent barriers to adoption, as well as the different paths asset managers may take to implementing tokenisation.

Tokenisation is a change of potentially seismic proportions for asset management – on a par with the emergence of ETFs in the 1990s and Internet trading around the turn of the century, and even the origination of the mutual fund in the 1920s. Yet it will not be an all-or-nothing transformation for most participants.

DLT offers a transparent and trustworthy infrastructure for performing the various tasks that make up asset management more efficiently. While wide-reaching use of this technology will be needed to unlock the full benefits of tokenisation, one advantage is that it lends itself to a modular approach – allowing asset managers to test, learn and optimise, proving value at each stage.

They may choose, for example, to start by launching tokenised funds in a particular asset class. Money markets funds have been one popular option: Franklin Templeton launched the first tokenised money market vehicle in 2021, and last year made it possible for shareholders in the fund to transfer their holdings peer-to-peer.[1] In November 2024, UBS launched a tokenised money market fund built on Ethereum.[2]

Such fund launches can help asset managers both to trial the practical implementation of DLT, and to explore some of the additional flexibility that tokenised funds offer. To use the example of money market funds, typically these are utilised by institutional investors for cash management, but cannot be used as collateral without first redeeming units and converting them back to cash. With a tokenised equivalent, investors could pledge their tokens to the counterparty as collateral without redeeming them, removing a series of cumbersome processes and allowing them to continue benefiting from the yield while the units are pledged.[3]

Calastone is working with firms to enable this through its Digital Investments solution, a digital platform that connects the various counterparties in a fund and helps firms to automate the tokenisation process to the click of a button, from what is traditionally a lengthy project. This network supports multiple blockchains and connects traditional fund processes with real-time tokenised asset movements, helping fund managers to begin unlocking the benefits of tokenisation in any asset class, including money market funds.

Another use case that has been explored is in settlements: last November, Citi and Fidelity International launched a proof-of-concept for a tokenised money market fund which could allow investors to settle multi asset positions across different currencies in real time.[4]

Ultimately, this is how the benefits of tokenisation will be realised: bringing one use case into production at a time, demonstrating how DLT enables asset managers to simplify and speed up key operational areas, or to extend their reach through new distribution venues. It is by aggregating all these improvements together that the full potential of tokenisation will be unlocked and the end state outlined in this report achieved.

An approach of many small steps is appropriate both for the scale of the task, and because some asset managers still hold reservations about tokenisation. When asked why they do not use DLT today, 55% highlighted deployment costs, ahead of 19% who highlighted a lack of feature benefits and 10% a deficit of internal expertise. Given that the technology stands to be significantly cost-saving, these fears suggest that there are still knowledge and experience gaps within asset management when it comes to tokenisation, and some distance for the industry to travel until it accepts the full scale of the transformation tokenisation may deliver and the associated benefits.

Ultimately, every asset manager will have a different path towards implementing tokenisation. They might begin by tokenising a single fund or asset class, or by focusing on a specific area of operations – be that to streamline settlements, automate fund accounting, or use DLT to distribute across new venues such as public blockchains.

They may choose to build teams in-house to do this, to work through third parties, or seek out partnerships with industry peers. And they may opt to focus initially on jurisdictions where regulation is favourable. The Citi/Fidelity money market proof of concept, launched under the auspices of the Monetary Authority of Singapore and its Project Guardian scheme, is one indicative example of collaboration under supportive regulatory conditions. In all cases, asset managers will be served by focusing on targeted areas of their business where tokenisation can make a tangible difference – demonstrating value and paving the value for broader adoption.

However asset managers choose to approach tokenisation, there is one fundamental truth that unites them. As this research makes clear, all face an unenviable set of circumstances whereby customers are seeking more choice and customisation, regulators are introducing new requirements, and the cost of doing business is going up and up. A technological leap is required to avoid profitability becoming squeezed between these competing demands.

Tokenisation can be that silver bullet, helping asset managers to move faster, realise substantial operational efficiencies and ultimately offer a more diverse, competitively-priced range of products to investors. As this research makes clear, the bottom line impact for the average fund, and the financial benefit to the industry as a whole, promises to be substantial. Moreover, tokenisation presents a future whereby asset management can divert from its collision course with wage inflation, implementing a highly scalable and efficient infrastructure that will reduce the traditional reliance on headcount. From the current trajectory where cost increases are assured, asset managers can start to work on the basis of cost reductions.

The long-term benefits of tokenisation are clear, which is not to say that the road to this end state will be short or straightforward. There are numerous challenges of implementation: asset managers need to have access to the right technical skills, they will need to overcome the limitations of legacy systems, and to find the right partners and providers.

Like all technological overhauls, tokenisation will involve a good degree of trial, error and learning. Calastone is committed to supporting that transition, providing a bridge between the current business model and a future in which we anticipate many asset managers will choose to run large parts of their business on DLT. Through Calastone Digital Investments, we offer the tools and expertise to support asset managers on the path to tokenisation – a framework to bring tokenised investment vehicles into production and realise immediate cost optimisations.

We envision a future where tokenisation is not an optional upgrade for asset managers but a foundational component of their strategy. As this research makes clear, DLT and tokenised funds deserve to be seen as essential tools to help asset managers deal with some of their most pressing challenges. In this light, tokenisation appears an opportunity too big to ignore, equipping the asset management industry to tackle challenges that are too urgent to delay.

[1] Franklin Templeton Announces Availability of Peer-to-Peer Transfers for Franklin OnChain U.S. Government Money Fund | TEMIT

[2] UBS Asset Management launches its first tokenized investment fund | UBS Global

[3] The future of tokenised yield-bearing assets as collateral – Calastone

[4] Citi and Fidelity International demonstrate tokenized Money Market Fund and Digital Foreign Exchange Swap solution