UK investors were brimming with confidence at the end of 2023, according to the latest Fund Flow Index from Calastone, the largest global funds network. December’s improvement in sentiment was evident across all asset classes: inflows to equity funds soared, fixed income funds saw increased inflows, buying of safe-haven money market funds dropped sharply and outflows from out-of-favour mixed asset and real estate funds pared back significantly.

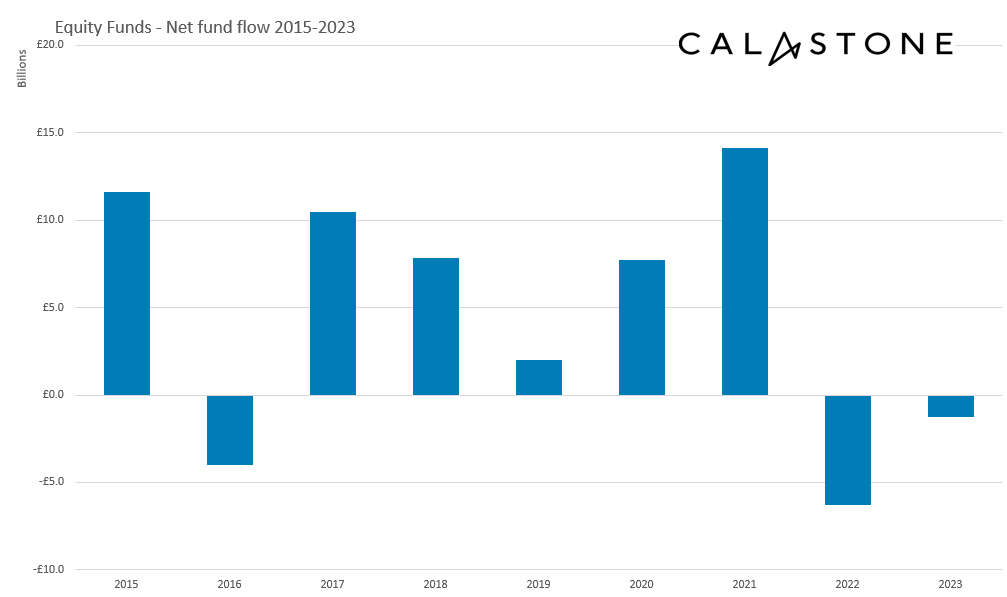

December inflows to equity funds surged to £1.19bn, making it the best month since April 2023

Inflows to equity funds soared to £1.19bn in December, making it by far the best month for equity funds since April 2023 and the second-highest level in almost two-and-a-half years[1]. Investors were especially enthusiastic on US equities – net inflows more than doubled in December to a record £968m. But the biggest turnaround came in European equities. Having withdrawn capital from the sector in every month since January 2022, investors added a net £476m to European equity funds in December, the second-best month on record[2]. Global funds and emerging markets all saw inflows too. Among geographical categories, only perennially unloved UK-focused equity funds saw outflows, though the £418m withdrawn was well below the monthly average for 2023 (-£667m).

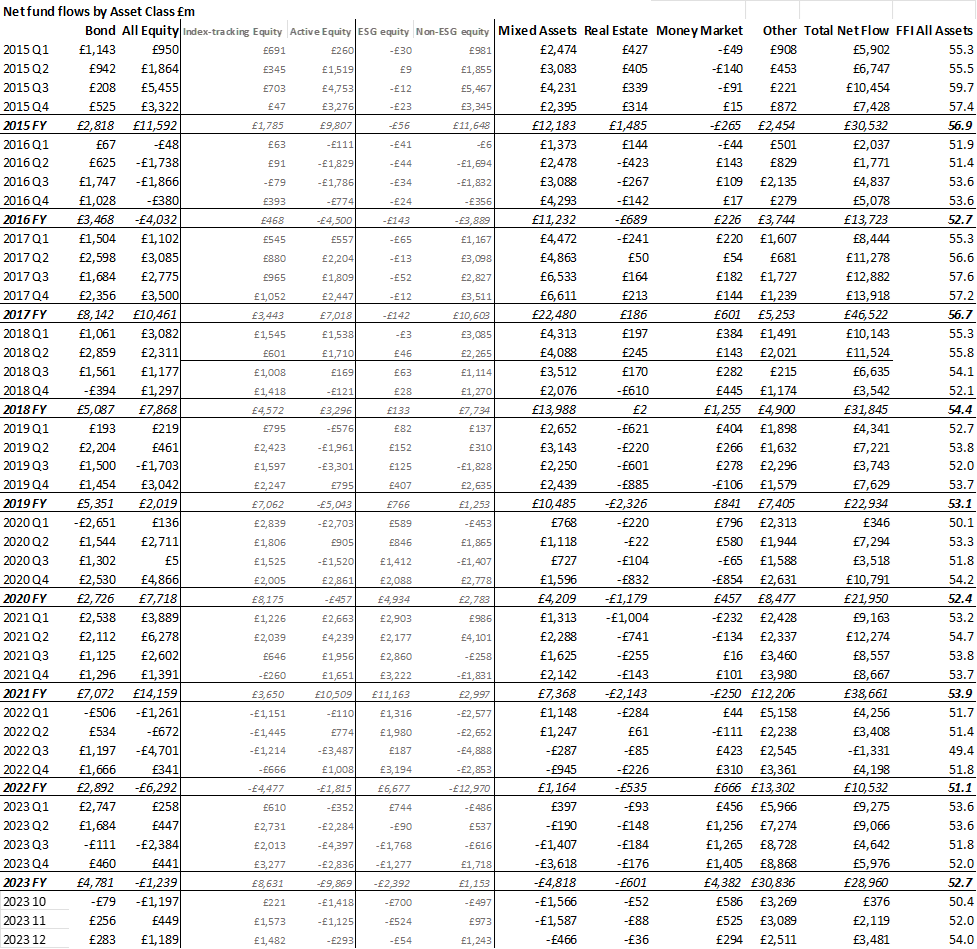

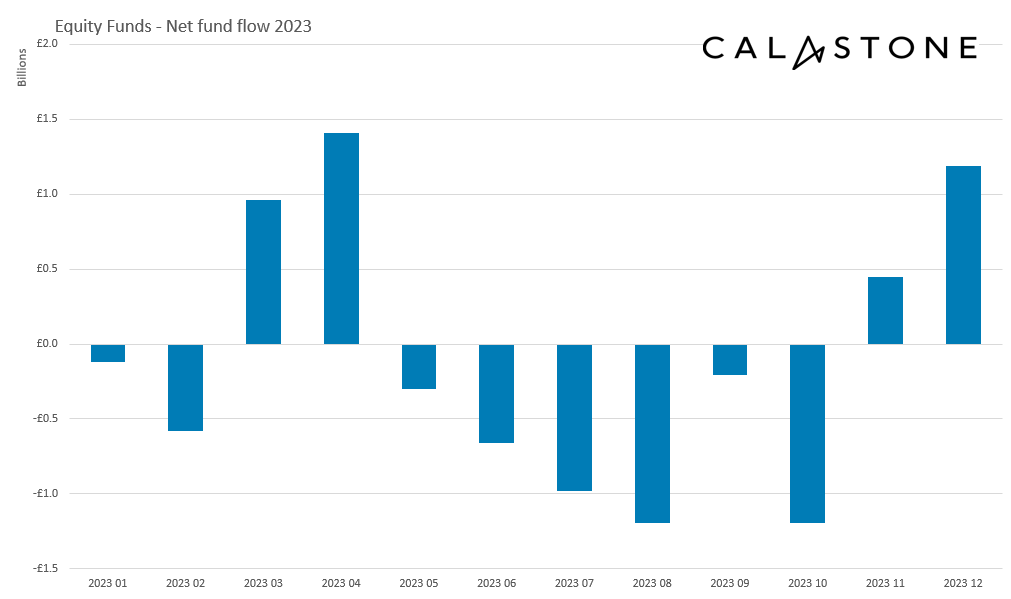

Overall, equity funds shed capital for second year running – thanks to unloved UK funds

December’s inflow to equity funds was not enough to prevent them suffering annual outflows for a second consecutive year, however. Volatile market conditions and economic uncertainty drove net outflows from the asset class in eight of 2023’s twelve months. For the whole of 2023, investors withdrew a net £1.24bn from equity funds. This was a significant improvement compared to 2022 (-£6.3bn) but meant that 2023 was another tough year for the fund management industry. Some categories have fared worse than others – 2023 marked the third consecutive year, and December the 31st consecutive month of outflows from UK-focused equity funds. Without the £8.01bn of outflowsfrom UK equities in 2023, all other kinds of equity funds between them attracted £6.77bn of new capital between them.

[1] April 2023 net inflow of £1.41bn; August 2021 net infw £1.25bn

[2] Record was December 2020, £509m.

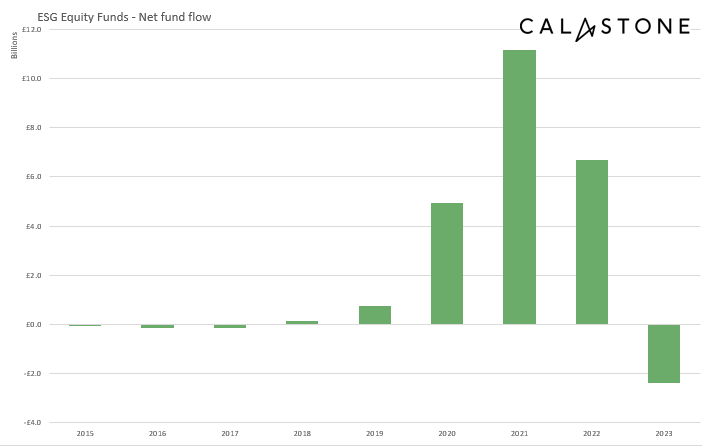

ESG equity funds hit by first year of net selling since ESG boom began in late 2019

ESG funds saw an eighth consecutive month of outflows in December, though at just -£54m, the net selling was the least severe since investors first turned negative on the ESG industry in May. Income and specialist sector funds also shed capital in December.

With £2.39bn of outflows during the year, ESG equity funds reversed just over one tenth of the inflows they have enjoyed during the ESG boom that began in late 2019.

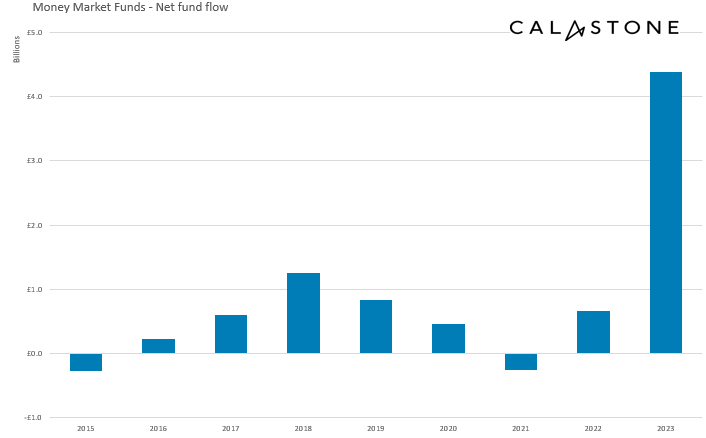

Money markets had their best year by far on record – inflows exceeded previous 8 years combined

Money market funds were big winners in 2023, absorbing a record £4.38bn of capital, more than in the previous eight years combined[1]. High interest rates and low risk attracted investors to money market funds in 2023. In December, when sentiment towards riskier assets rose sharply, inflows to money market funds fell to £294m, well below the average inflow of the previous six months[2].

[1] 2015-2022 £3.53bn inflow

[2] May to Nov 2023 Money Market fund average monthly inflow £480m

Fixed income fund inflows returned at the end of 2023 as bond markets recovered strongly

Fixed income funds saw inflows rise in December to a net £283m as investors became increasingly convinced that the interest-rate cycle in the US, Europe and the UK has now peaked. The full year picture was mixed, however. A very strong start saw inflows of £4.67bn between January and July, putting 2023 on course to be a record year for the asset class. But this petered out over the summer and early autumn. Investors only returned with relative caution to fixed income funds in November and December, and for the second half of the year overall, almost no new money flowed into the asset class. £4.78bn of inflows in 2023 were exactly in line with the long-run average in the end.

Among other asset classes, mixed asset fund outflows reduced to £466m in December, down from £1.59bn in November. 2023 was the first year on Calastone’s record to see net outflows from the asset class – totalling £4.82bn. Property funds also fared badly with a fifth consecutive year of outflows. 2023 saw them shed £601m.

Edward Glyn, head of global markets at Calastone said: “The bond markets are still firmly in the driving seat. After the bear market of 2022, investors started the year by trying to lock into high bond yields and the capital gains that would eventually flow from expected disinflation. Investors also piled into equities, banking on a rally. That all made sense at the time, but then bond markets detoured into extreme pessimism in the middle of the year over the feared inability of higher interest rates to quell inflation. Yields soared even higher – this put capital markets under strain since all asset valuations depend on bond yields, it turned the thumbscrews on government and company finances, and it damaged confidence in the economy.

“The last couple of months have seen a dramatic turnaround both in the markets and in fund flows as evidence of disinflation is showing up all over the place – and that means rates might next move downwards. Equities are back on the buy list and that very same fixed income trade – lock into high yield and look for capital gains – is back in vogue too.

“Money market funds are doing well for two reasons. First, they are a safe haven as they invest in very short-dated fixed income securities – such bonds redeem within weeks, so credit risk is minimal, and yields are high just now. And secondly, the yield on money market funds is often well above what is available for cash on deposit at a bank, so they are drawing money away from the banking sector that might otherwise have idled in instant access savings.

“The outlook for 2023 is unusually unclear. Many central banks are reluctant to signal rate cuts are coming, though the markets are ignoring them for now. The extent of the economic slowdown in the UK and Europe, and whether the red-hot US can engineer a soft landing are also crucial to the outlook for asset prices – and fund flows.”