Asia’s economic outlook has improved in 2024, with growth projections revised upwards to 4.5% in 2024[1] and inflation slowly moderating. While positive, material risks remain as the investors continue to navigate the ongoing turbulence of geopolitical uncertainty, supply chain disruptions, property market defaults and slowing demand for critical commodities. Against this backdrop, investors in Asia have shown ‘cautious optimism’ in returning to the market, with net inflows in H1 2024 across all asset class fund categories more than 1.5x the total recorded in all of 2023. That being said, according to the latest fund flow data from Calastone – the largest funds network in Asia with over 10 years of operation in the region – capital flows have been dominated by rising allocations to fixed income funds as portfolio stability and income remain top of mind for investors.

Surge in fixed income funds investment as investors eye rate cuts

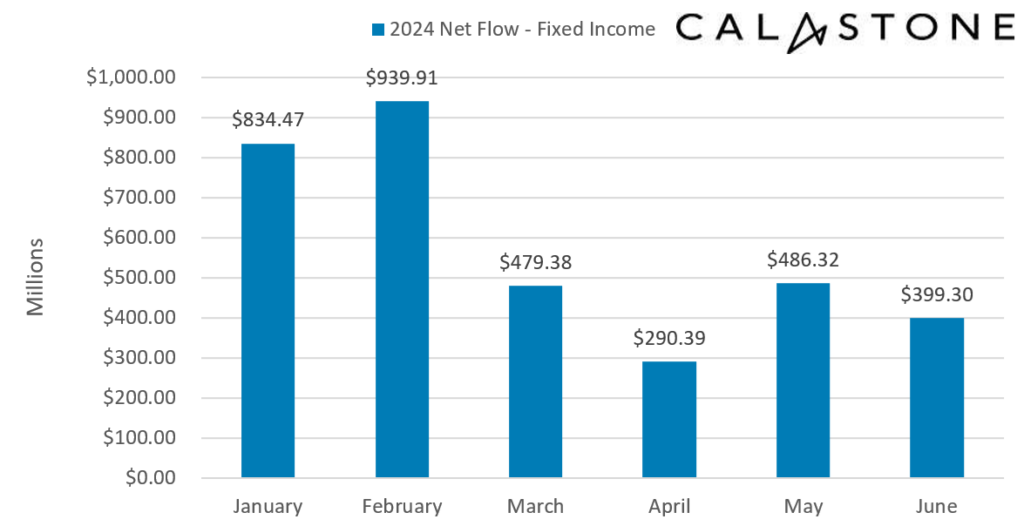

Investor interest in fixed income has remained strong throughout H1 2024 as investors sought to lock in yields and weigh bets for the timing of interest rate normalisation from central banks around the world, including the US Federal Reserve. Capital inflows from investors in Asia saw accelerated momentum in the first half of the year, with investments into fixed income strategies totalling US$3.3 billion on a net inflow basis. This is in sharp contrast to the modest net inflow of US$1.7 billion recorded in H1 2023.

January and February stood out with the highest volume of net inflows this year (totalling US$1.8 billion), coinciding with the two largest months of outflows from equity funds. The shift in investor behaviour points towards continued portfolio rebalancing in favour of stability and income in the current interest rate and market environment. Looking closer at the data, the rest of the period saw more moderate inflows, averaging $392 million per month, as widely held expectations for an impending rate cut got pushed out later into H2 2024.

Net buying of equity funds returns in late H1 2024

The first quarter of 2024 started the year off on a challenging note for equity funds, with net outflows totalling US$439.7 million, continuing a trend of net redemptions and risk-off positioning by investors in Asia that started in April 2023. However, May and June recorded the first months of net inflows for fund managers in more than 12 months, which could be explained by growing optimism around a near-term interest rate cut, as well as growing expectations of a soft landing for the global economy into 2025.

Justin Christopher, Head of Asia at Calastone, commented on the shift towards fixed income, stating: “Analysing real-time transaction data on our platform shows investors in the region still have a strong preference for opportunities that can help insulate their portfolios from market shocks and uncertainty. In the current environment, fixed income fund managers have been a clear beneficiary of capital flows over the last 18 months, but we are starting to see flows broaden out back into equities as the ‘fear of missing out’ grows with global stocks grinding higher.”

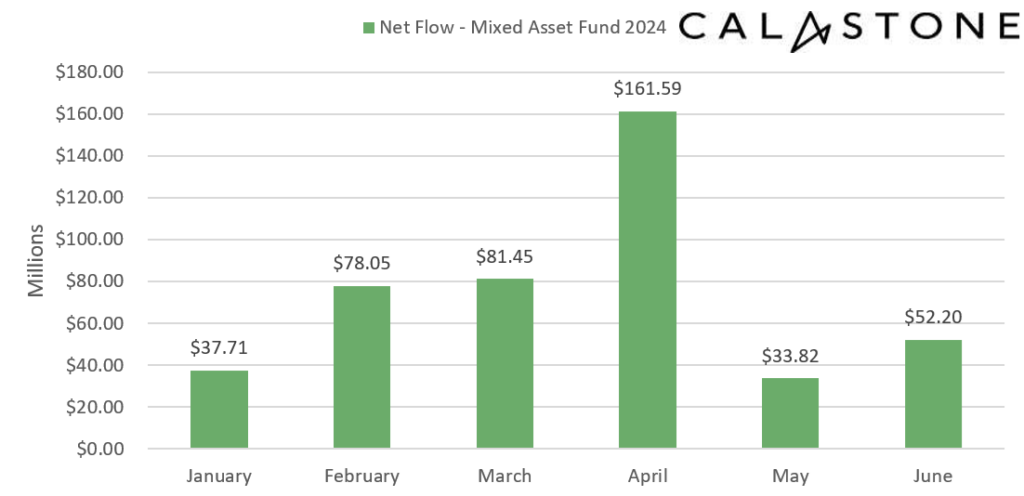

Mixed asset funds show resilience with consistent inflows as investors seek diversified portfolios

Funds with a mixed asset strategy recorded steady inflows during the first half of 2024, with subscriptions from investors amounting to US$444.81 million on a net inflow basis. Most notably, investors slowly increased contributions to these strategies into April, likely in anticipation of a mid-year Fed rate cut, before paring back some of this enthusiasm in the later part of Q2 2024. While there are some variations in the pace of investment activity as sentiments wax and wane with the economic cycle, it is important to highlight the relative stability of investment inflows for this fund category. The central role these funds play in regular retirement and savings plans for individuals means contributions are not often used to speculate on short-term market outlooks. In fact, despite ongoing uncertainty, these strategies have consistently drawn inflows from investors over the last year and a half, with only three months where redemptions exceeded subscriptions.