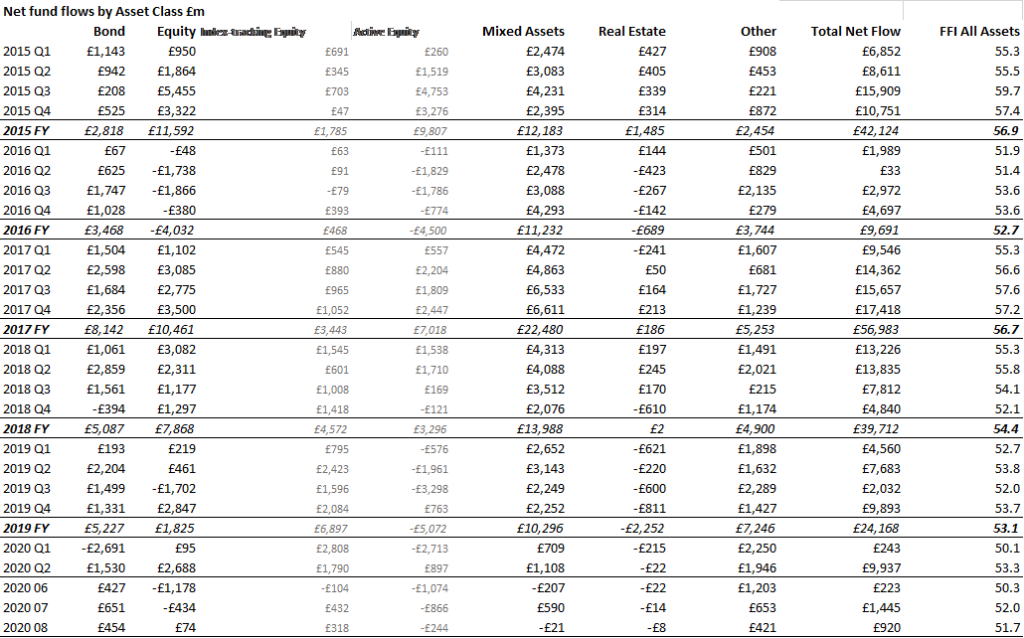

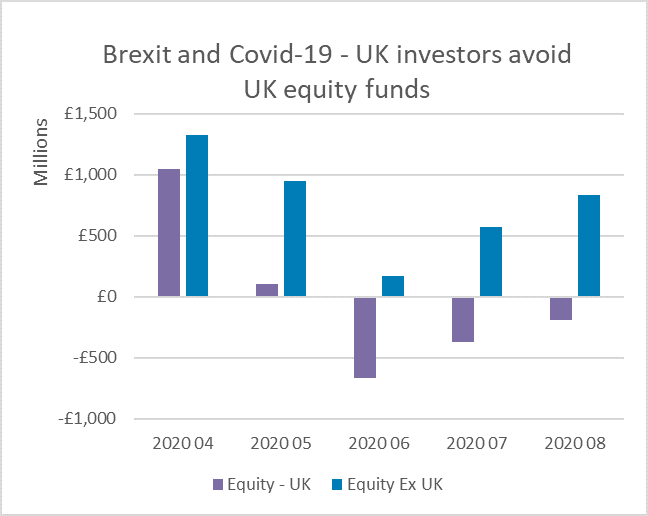

Investors are punishing UK equity funds as a no-deal Brexit once again looms large on the horizon, adding to the pain caused by the UK’s position at the bottom of the OECD economic league for its performance during the lockdown.

The latest Fund Flow Index from Calastone, the largest global funds network, shows that a net £1.2bn has flooded out of UK-focused equity funds between June and August, since the UK government set the country on course for a disorderly exit from the Brexit transition period by refusing to request an extension. This has been the worst three-month period of outflows from UK-focused equity funds on Calastone’s record[1], even worse than in the direct aftermath of the Brexit referendum. In complete contrast to UK funds, since June other flavours of equity funds (ie those without a specific UK focus) have enjoyed their second-best three-month period in almost two years – between June and August, investors added £1.6bn to their non-UK holdings. UK funds have now done worse than those investing elsewhere for five months in a row.

No other single category of equity funds has seen outflows anything like those experienced by UK funds in the last three months. Equity income funds are the one exception, but in truth they only reinforce the trend because they are so heavily weighted to UK equities. They too have had their worst ever three-month period. Analysis of Investment Association data suggests that approximately three quarters of equity income funds by value are primarily focused on UK equities. This suggests that a further £1.4bn[2] of outflows therefore represent investor distaste for UK assets, adding to the £1.2bn leaving funds specifically labelled UK.

Active UK equity funds have been especially hard hit by the reversal of sentiment. Half the outflows from active funds in the last three months are attributable to UK equity funds alone.

Just as UK funds reach a new nadir on investors’ wish-lists, European equity funds may finally be emerging from the doghouse. August data suggests European equity funds may have staunched the outflows that have dogged them every month for the last two years. August saw £170m of net inflows, the first time investors have added new capital to European funds since September 2019. This followed a July that saw the lowest outflow since November 2019.

Edward Glyn, head of global markets at Calastone said: “Not content with the economic storm caused by the pandemic, the prospect of a no-deal Brexit is once again clouding the outlook for the UK too. This is prompting investors to dump their UK holdings and switch to markets showing greater Covid-19 resilience and that don’t face Britain’s bespoke Brexit risks.

On the face of it, the inflow to European funds seems strange given rising infection rates but European equities are relatively cheap compared to their record-priced US counterparts and the dollar is in decline. Funds focused on US equities had one of their worst months in the last year in August so investors may be switching focus as a hedge against the political, social and economic upheaval in the US, though we will need to see several more months of solid inflows to Europe before we can be sure this is a new trend. Low valuation alone is not enough to tempt investors as unloved UK equity funds can testify.”

No other single category of equity funds has seen outflows anything like those experienced by UK funds in the last three months. Equity income funds are the one exception, but in truth they only reinforce the trend because they are so heavily weighted to UK equities. They too have had their worst ever three-month period. Analysis of Investment Association data suggests that approximately three quarters of equity income funds by value are primarily focused on UK equities. This suggests that a further £1.4bn[2] of outflows therefore represent investor distaste for UK assets, adding to the £1.2bn leaving funds specifically labelled UK.

Active UK equity funds have been especially hard hit by the reversal of sentiment. Half the outflows from active funds in the last three months are attributable to UK equity funds alone.

Just as UK funds reach a new nadir on investors’ wish-lists, European equity funds may finally be emerging from the doghouse. August data suggests European equity funds may have staunched the outflows that have dogged them every month for the last two years. August saw £170m of net inflows, the first time investors have added new capital to European funds since September 2019. This followed a July that saw the lowest outflow since November 2019.

Edward Glyn, head of global markets at Calastone said: “Not content with the economic storm caused by the pandemic, the prospect of a no-deal Brexit is once again clouding the outlook for the UK too. This is prompting investors to dump their UK holdings and switch to markets showing greater Covid-19 resilience and that don’t face Britain’s bespoke Brexit risks.

On the face of it, the inflow to European funds seems strange given rising infection rates but European equities are relatively cheap compared to their record-priced US counterparts and the dollar is in decline. Funds focused on US equities had one of their worst months in the last year in August so investors may be switching focus as a hedge against the political, social and economic upheaval in the US, though we will need to see several more months of solid inflows to Europe before we can be sure this is a new trend. Low valuation alone is not enough to tempt investors as unloved UK equity funds can testify.”